Summary

I have discussed the Yen Carry Trade and the Samurai bond market many times over the years. Samurai bonds are a component of the Yen Carry Trade, and fund many of the activities of the US Financial sector.

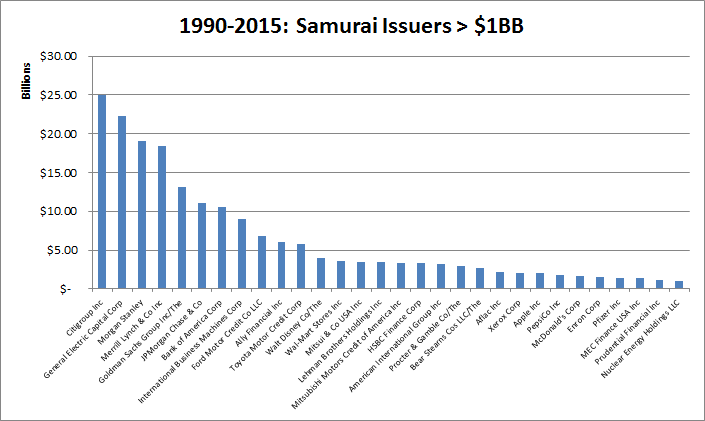

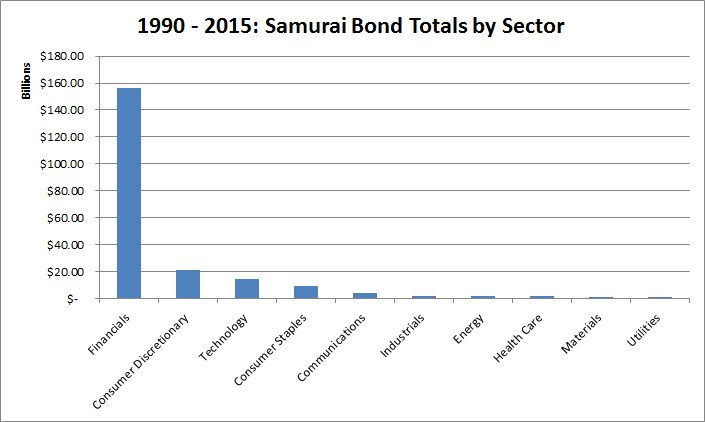

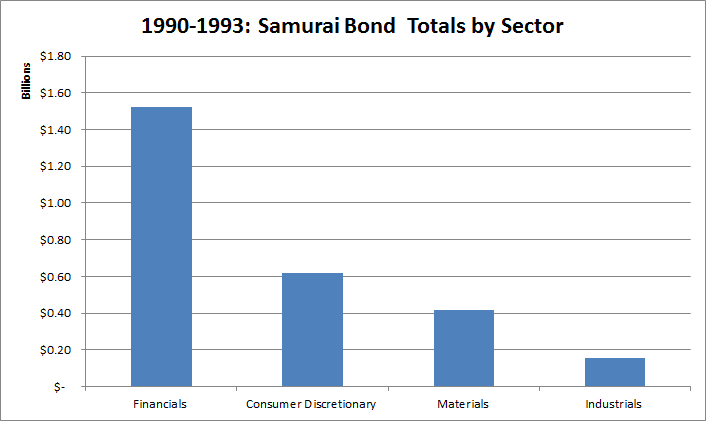

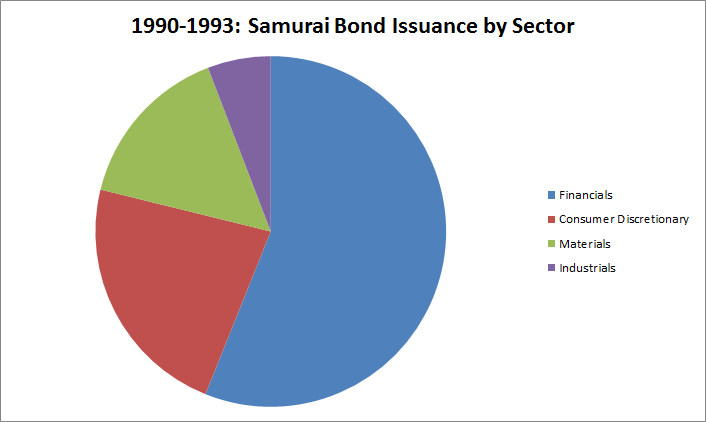

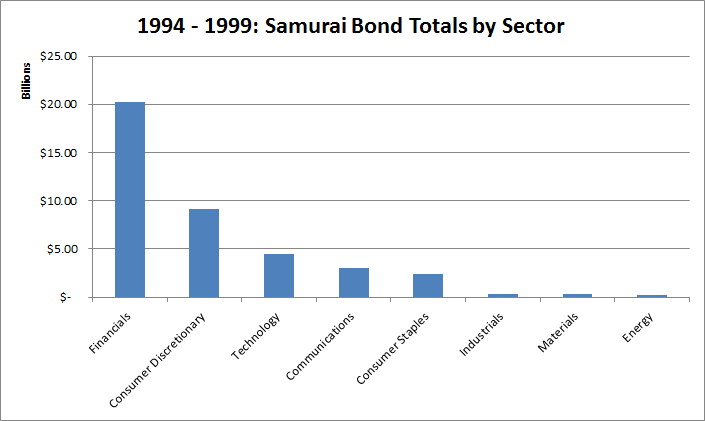

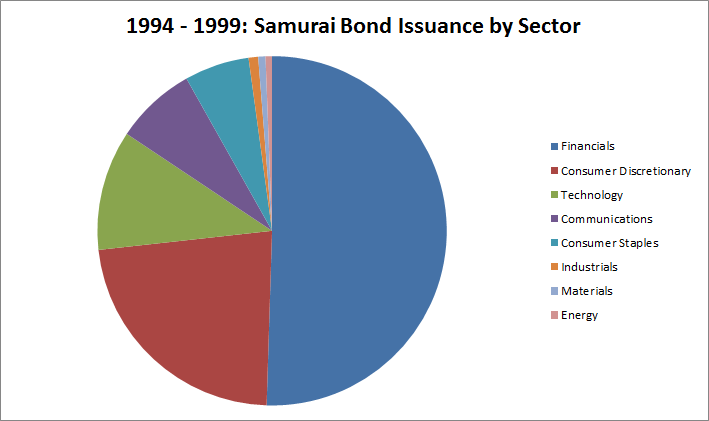

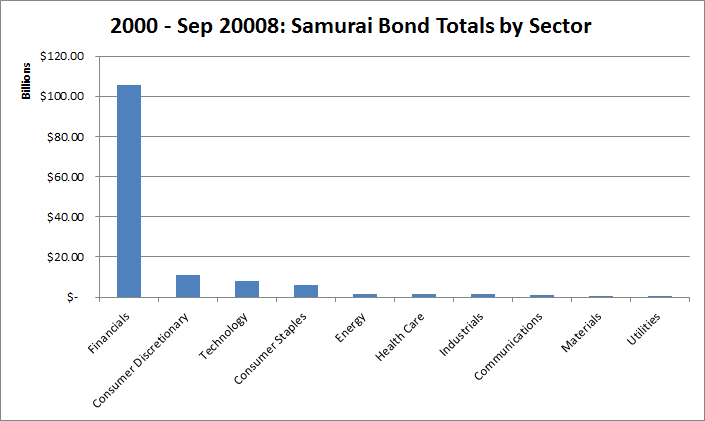

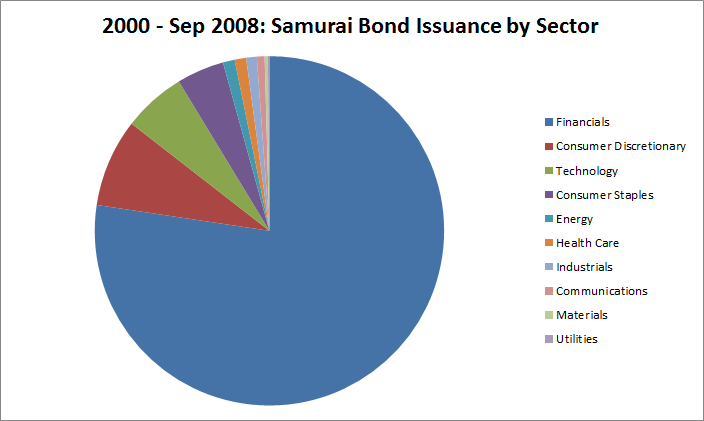

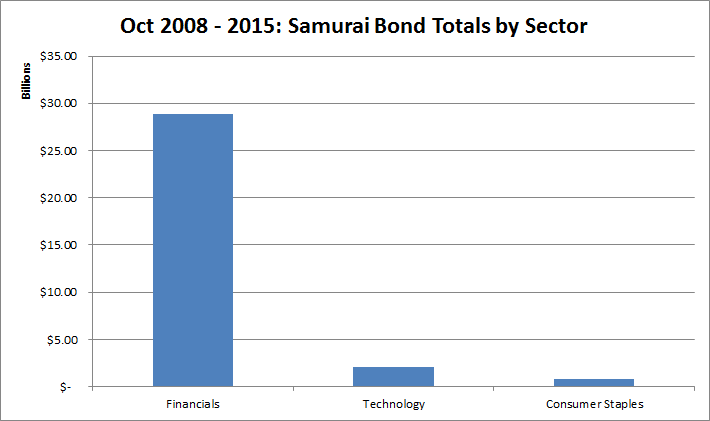

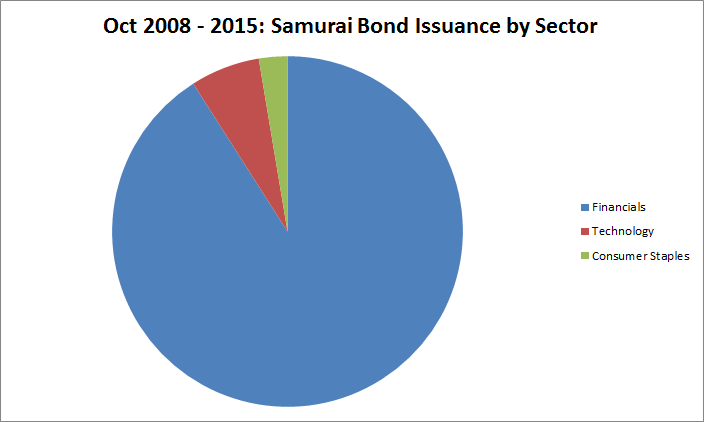

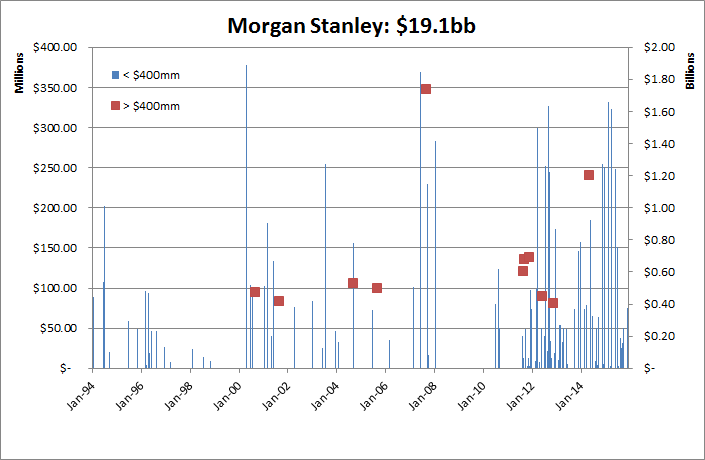

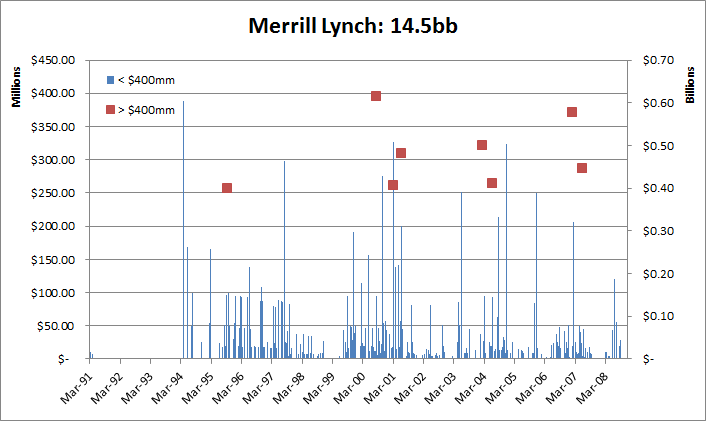

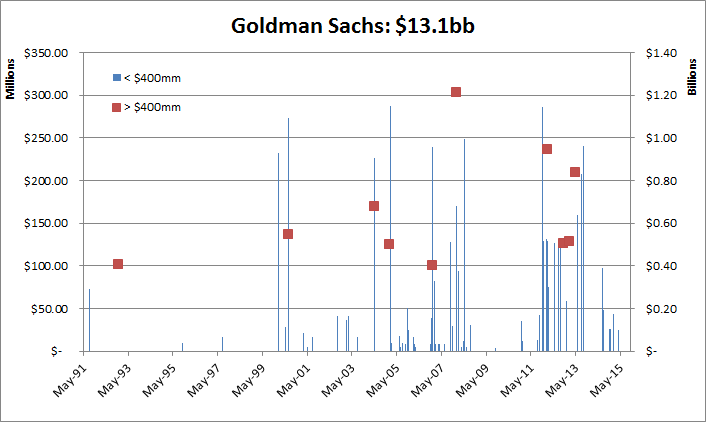

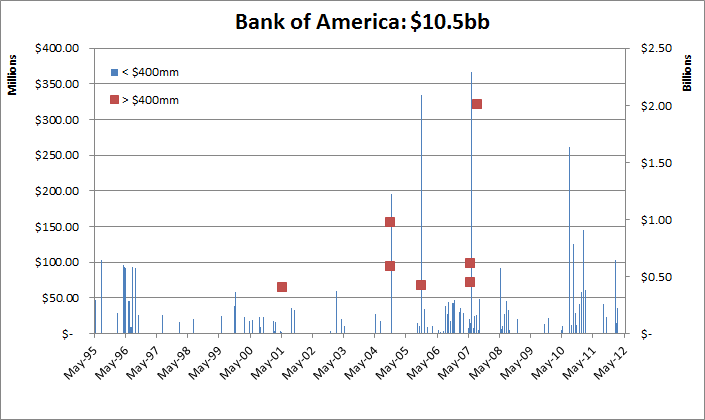

The dominant sector using the Samurai bonds is Finance, and I suspect much of this debt counted as capital for most of the issuers. Since financial firms operate with very high leverage, the multiplier effect of this debt cannot be ignored.

This study contains a lot of data that is not commonly known. It provides evidentiary support to the analysis I perform in a forthcoming study of the Carry Trade. As I will discuss in the article on the Carry trade, the Samurai bond market has been an important component in the Failure of domestic Monetary Policy by the central banks.

The Samurai Bond Market is important to monitor in the context of the Global Financial Crisis, as it funded many of the excesses in the periods leading to the collapse in the markets. It continues to be relevant today.

A Brief History

Samurai bonds refer to debt instruments sold in Japan by foreign issuers. Typically, they are issued by US corporations, but they are also issued by Japanese institutions that might have operations in the US, such as Banks, and financing arms of Automobile Manufacturers. Sovereign nations also sometimes issue Samurai bonds.

The euroyen market is also another source of borrowing for issuers, but starting in the 1990s, the samurai market began dominating the euroyen market.

While there was some research on Samurai bonds done in the 1990s, most of it focused on the credit risk and pricing of these bonds (especially after the elimination of the minimum rating requirement), as the majority of the purchasers were individuals. I have yet to find any research that connects the Samurai bond markets to the Yen Carry trade, or any analyses of the impact this market has had on borrowing nations.

Some of my numbers and information come from 2 articles by Frank Packer (both linked below). Most of my quotes are also from the Packer articles.

Samurai bonds are permitted by the Ministry of Finance to “facilitate the recycling of Japan’s trade surplus”. “As policies were liberalized, in an effort to increase the use of Yen as an international currency”, issuance picked up, with lower rated borrowers also getting access.

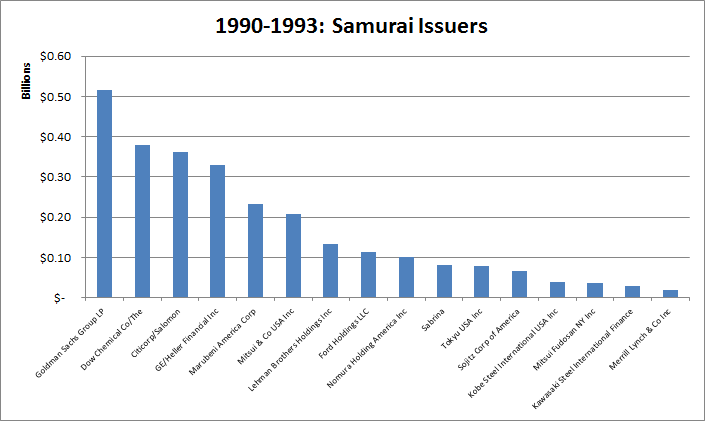

The first issuance was by the Asian Development Bank in 1970. The first sovereign issue was in 1972 for Australia, and the first private issue was in 1979 for Sears Roebuck.

Data Source: Bloomberg.

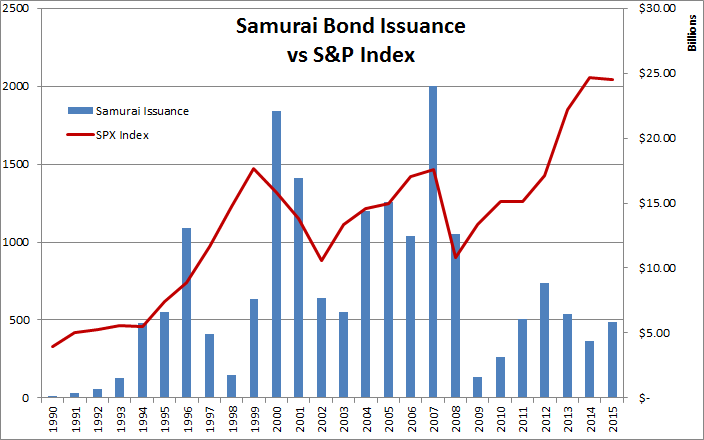

I do not have data earlier than 1990; in any case, I am only interested in the periods leading up to and after the initiation of the Yen Carry Trade in 1994.

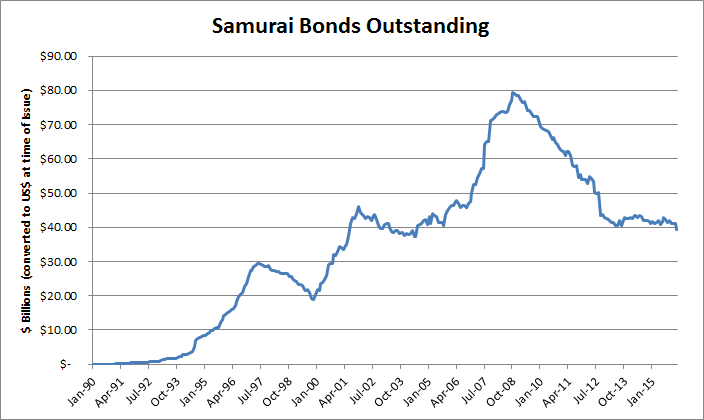

Samurai Issues from 1990 to 2015

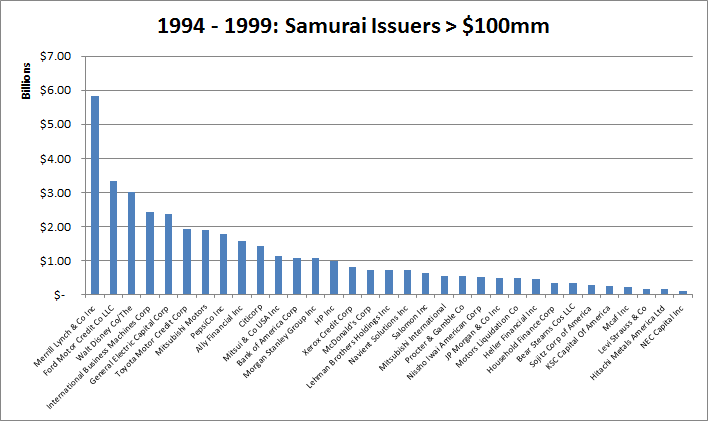

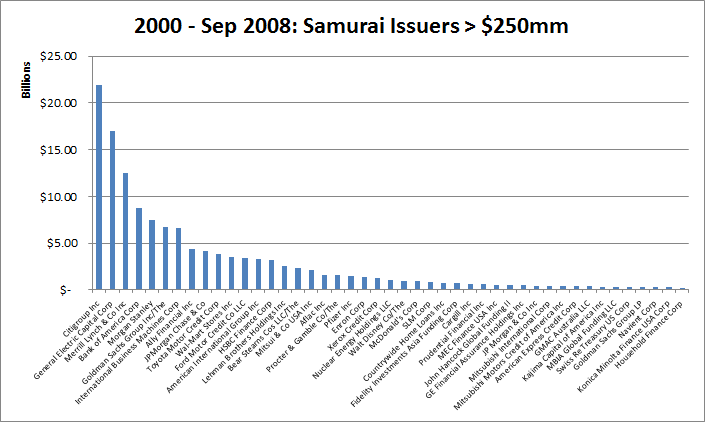

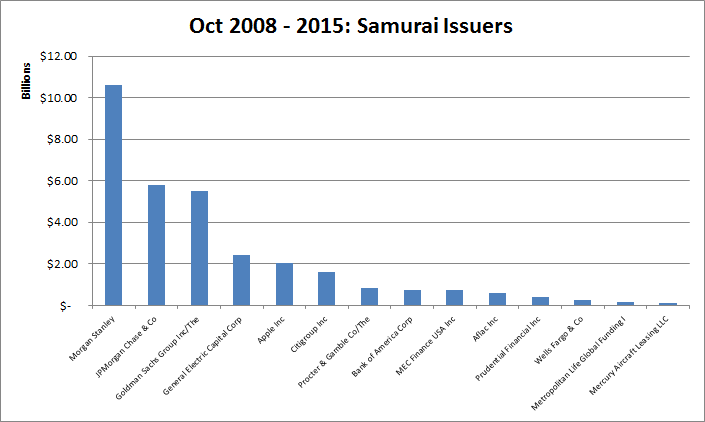

Since 1990, there have been almost 3000 issues, totaling over $210BB, by approximately 132 issuers. (I am missing the issuance size data for 12 issues.) I have also tried to consolidate related names, for example, combining AIG wih AIG Financial Products. As I mentioned, Finance has been the dominant sector.