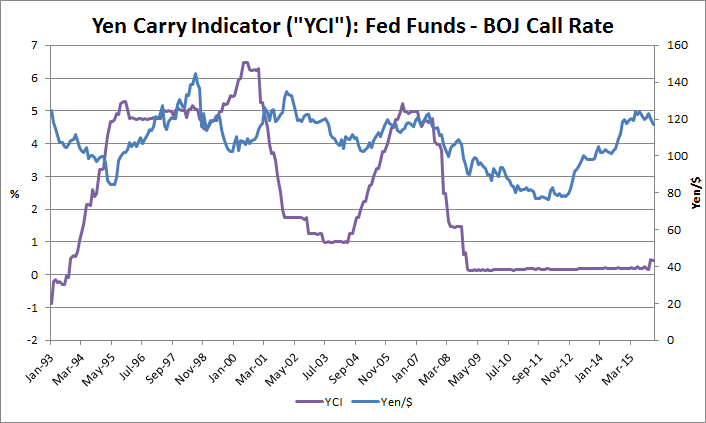

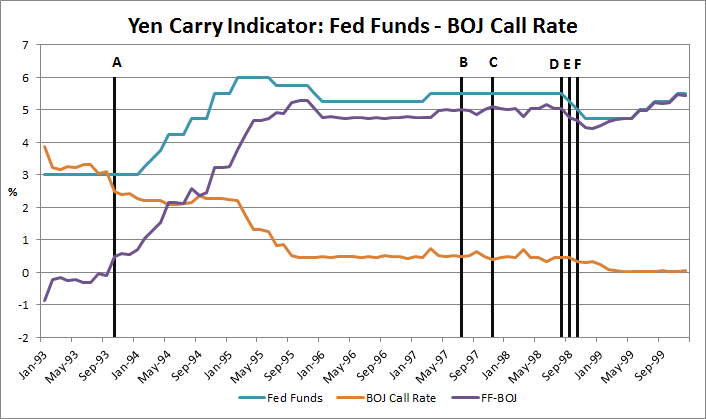

Section 1: Carry Trades

Section 1: Carry Trades“Carry Trade” is the term given to borrowing money in a low yielding currency (i.e. country), and investing the proceeds in the currency and assets of a higher yielding country, thereby earning a net spread, or carry.

Carry trades should never exist, as the economic concept of “Interest Rate Parity” should prevent any arbitrages from occurring. However, they do exist and are the most powerful force in Finance and Economics, as they thwart attempts by Central Banks to conduct monetary policy. The world as we know it today (since the early 1990s) has been sculpted by Carry Trades, and almost all asset prices are a result of asset inflation (and deflation) from deployment (and withdrawal) of Carry Leverage.

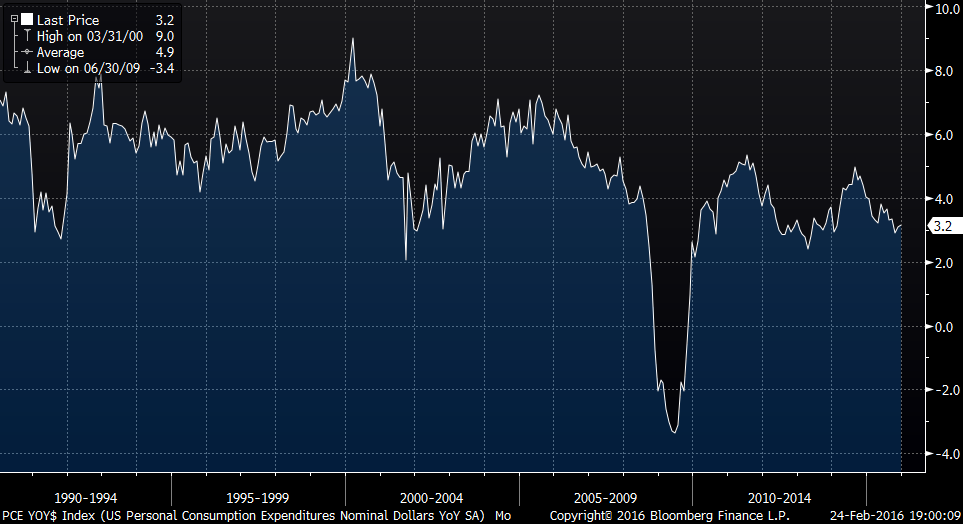

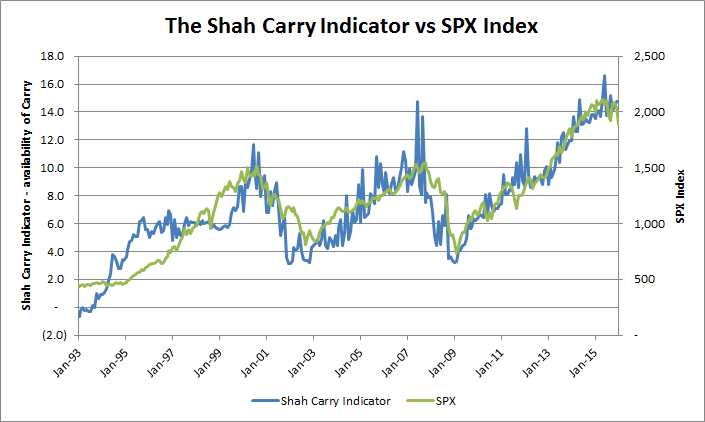

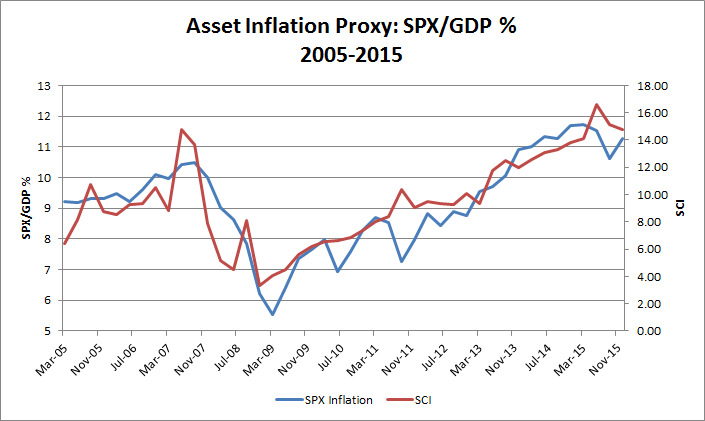

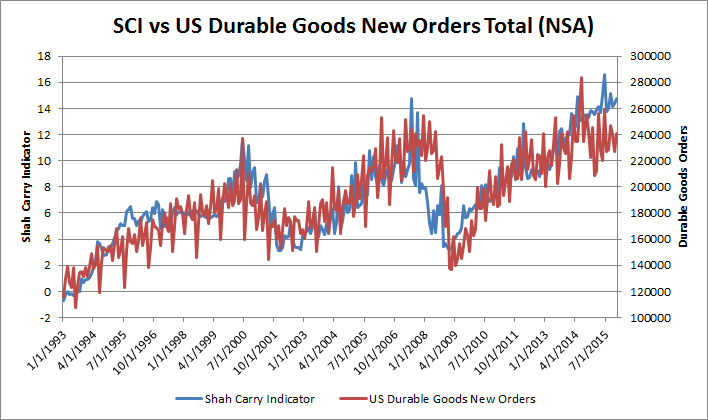

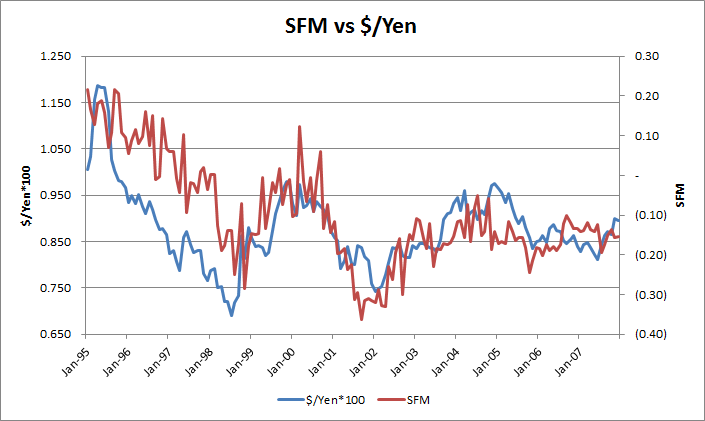

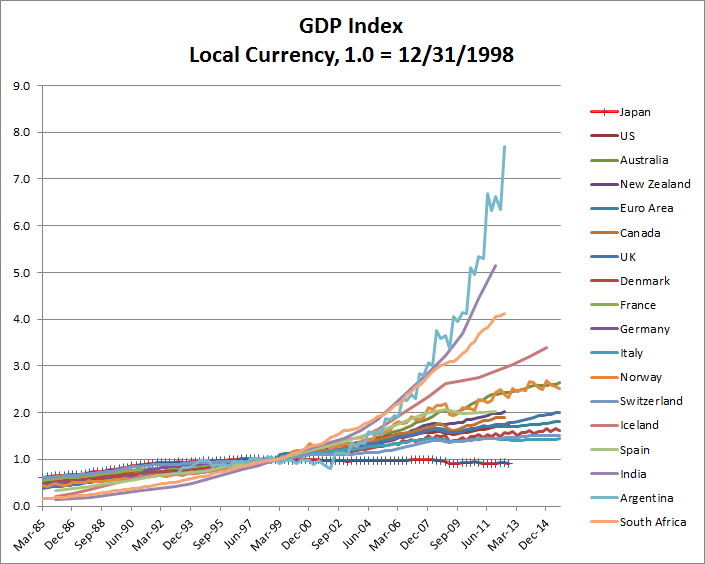

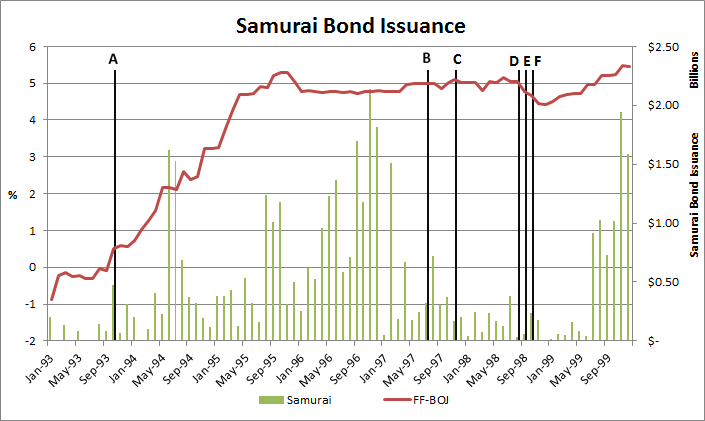

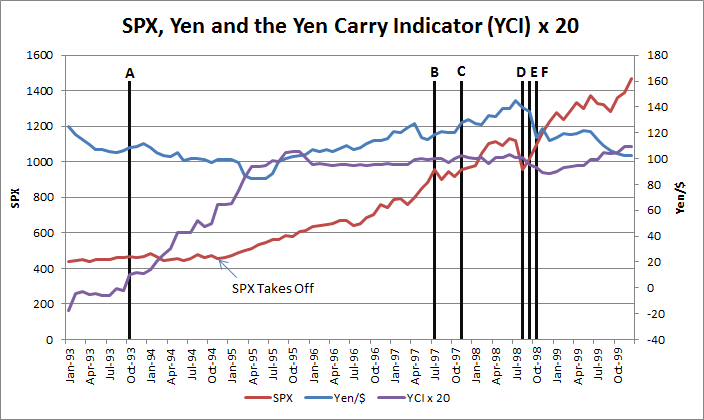

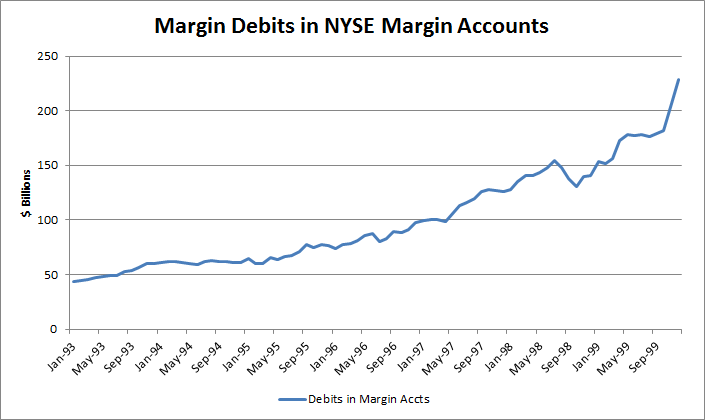

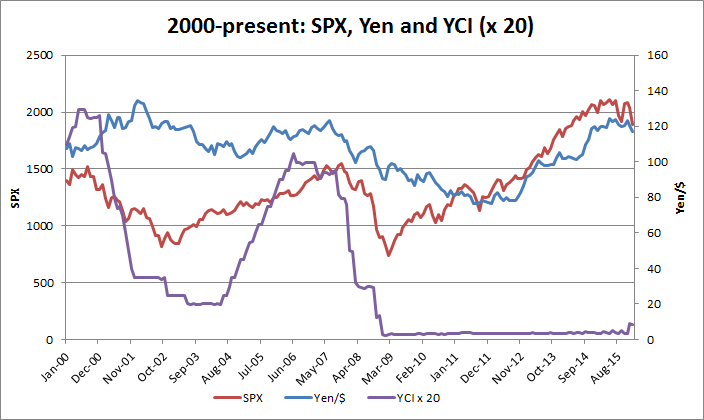

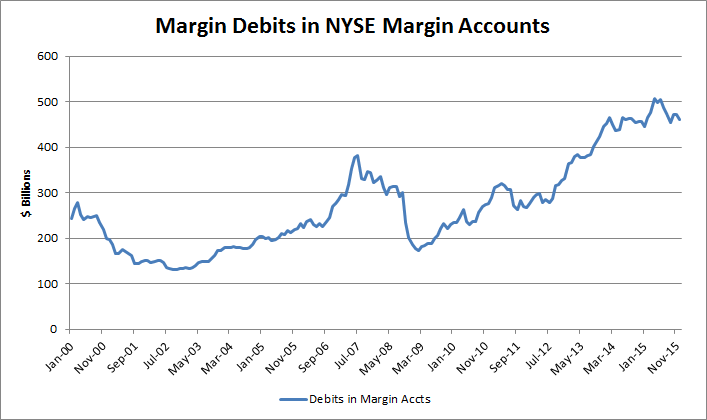

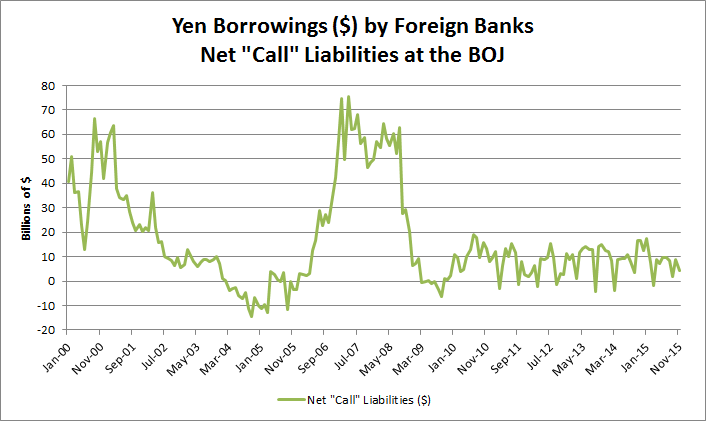

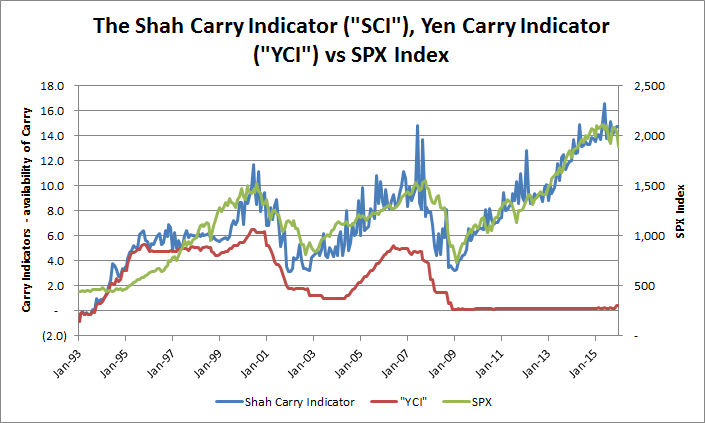

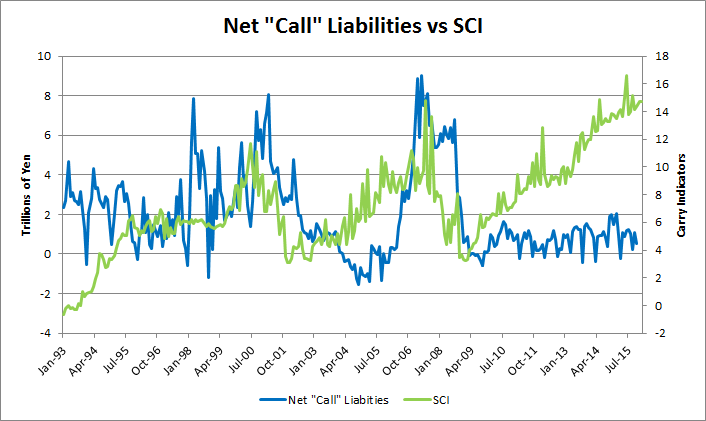

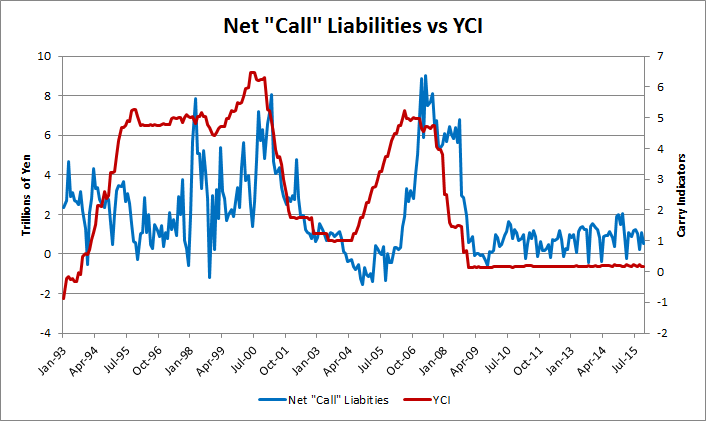

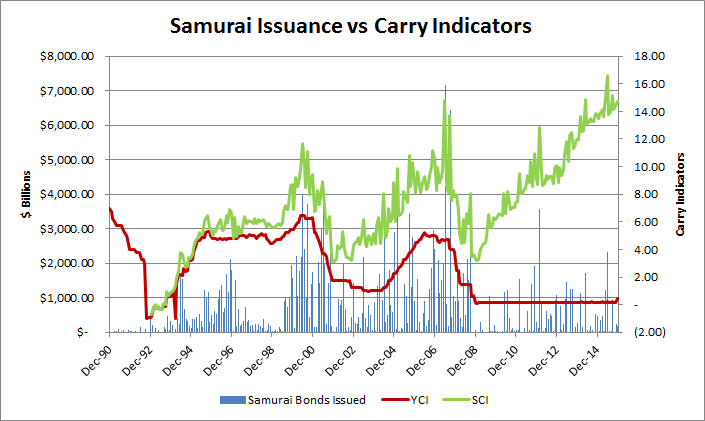

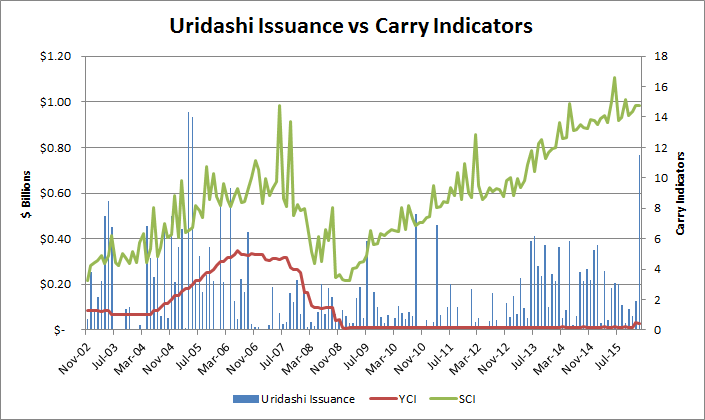

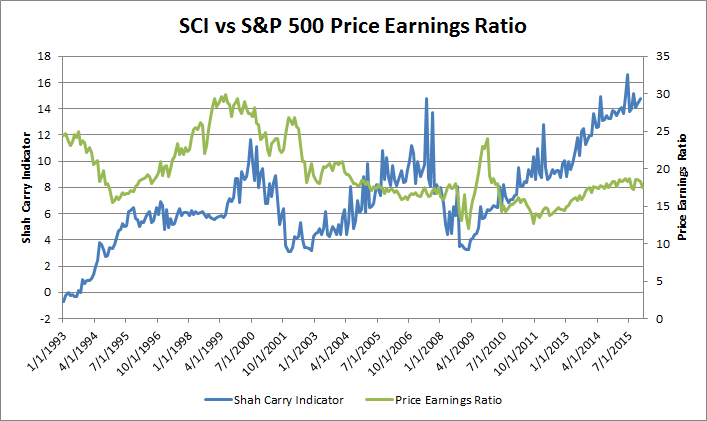

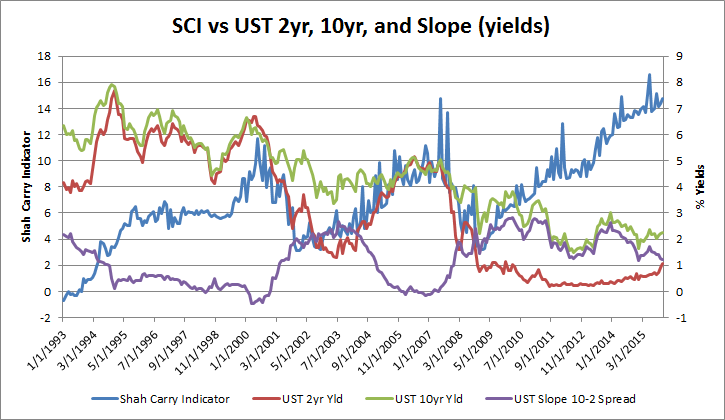

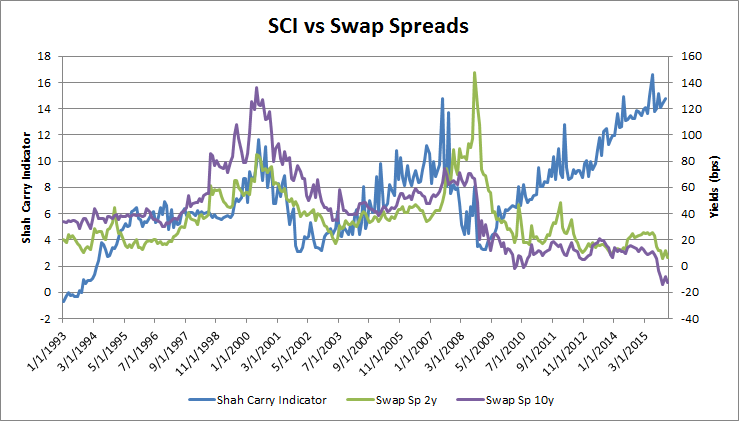

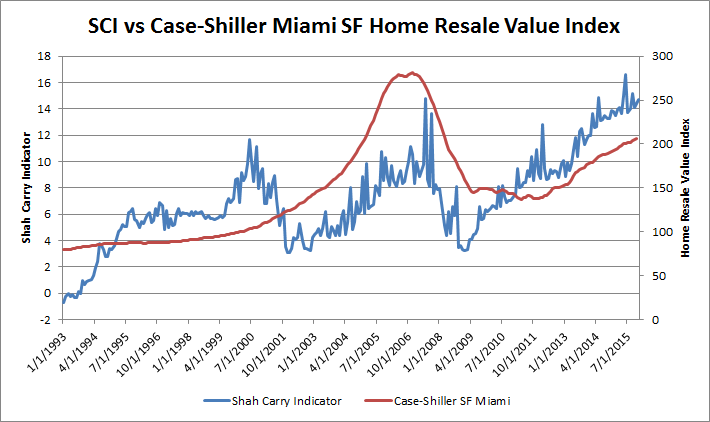

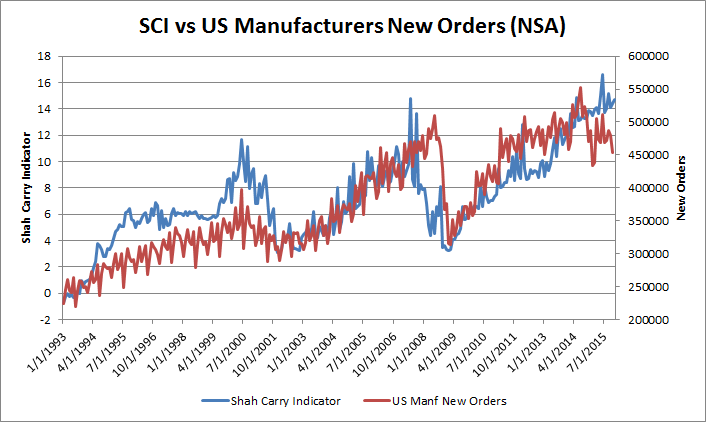

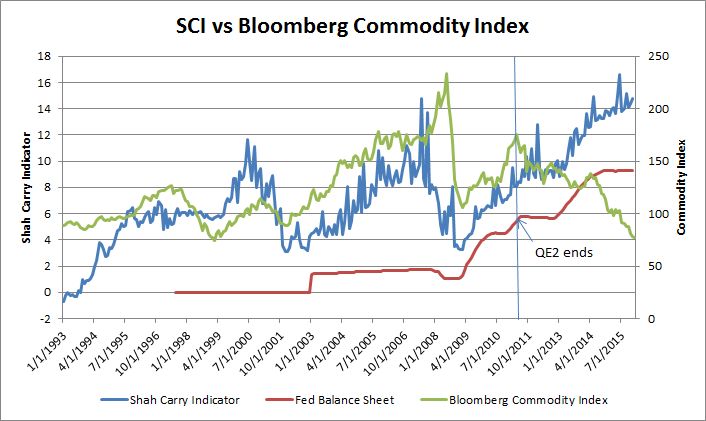

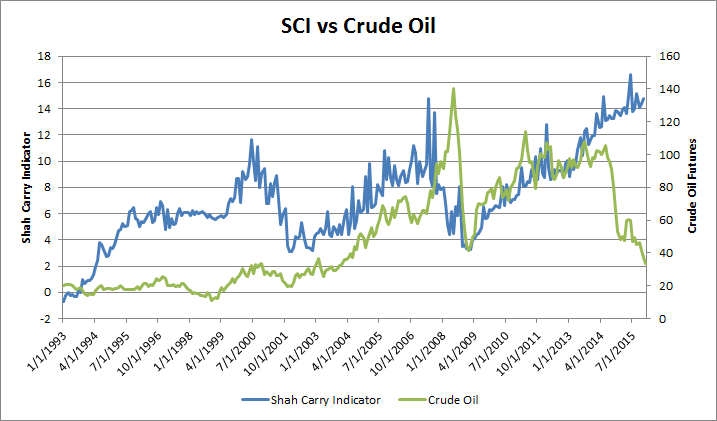

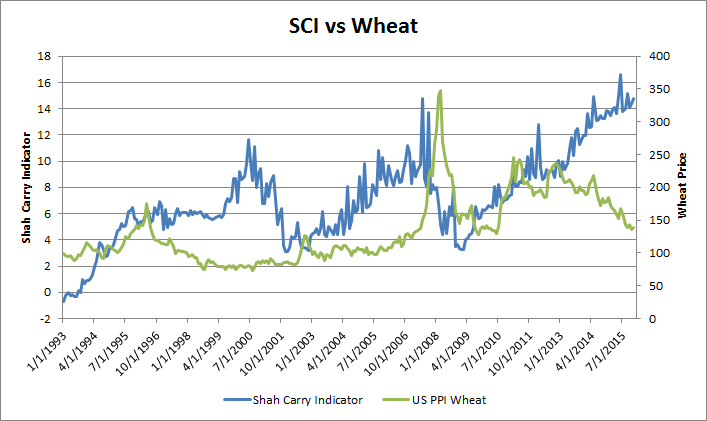

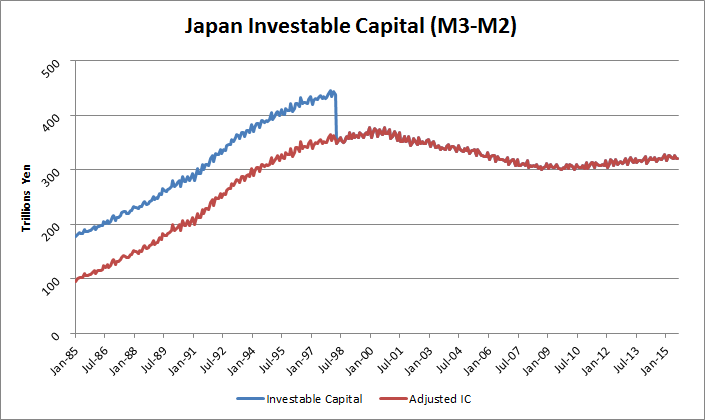

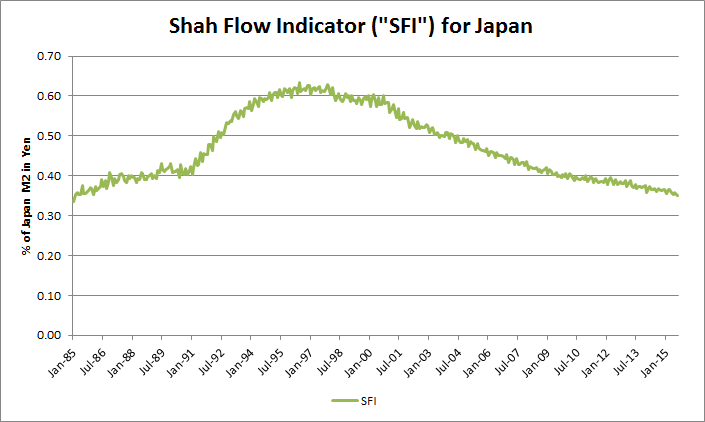

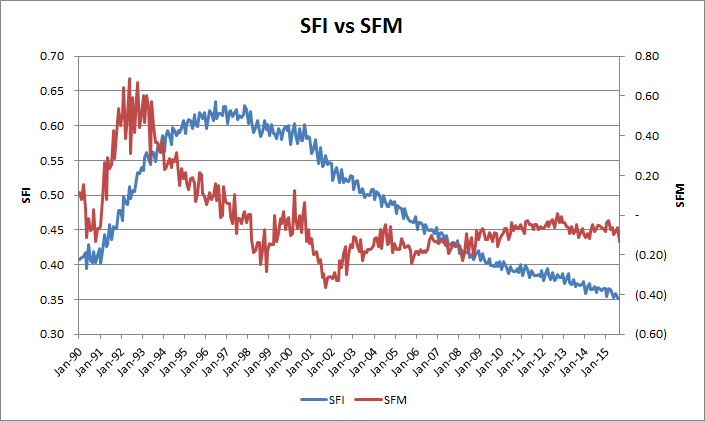

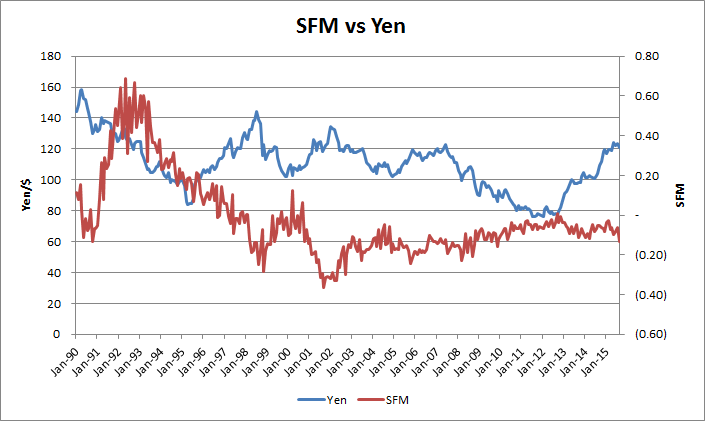

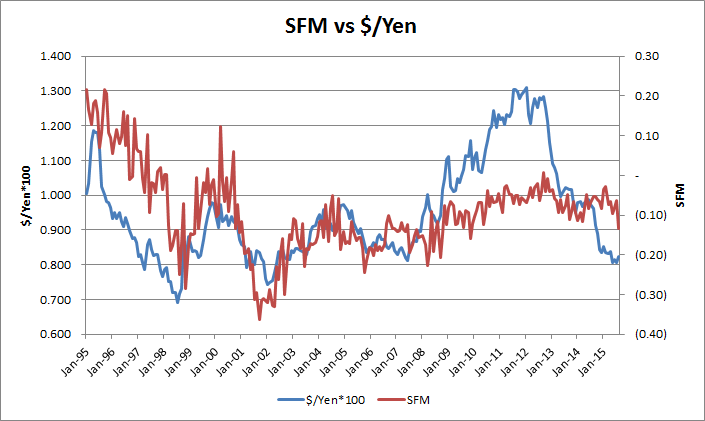

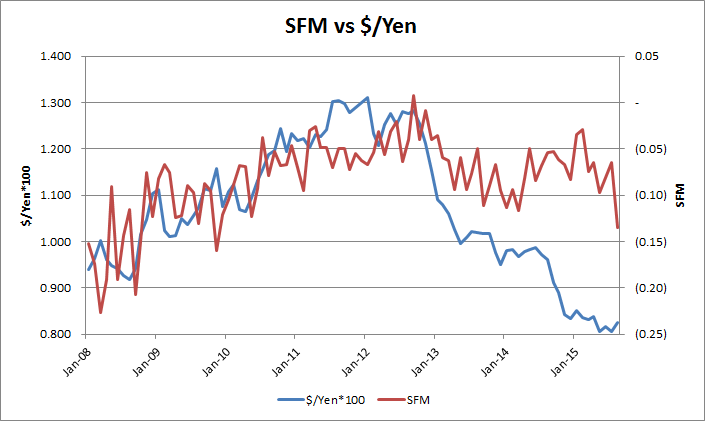

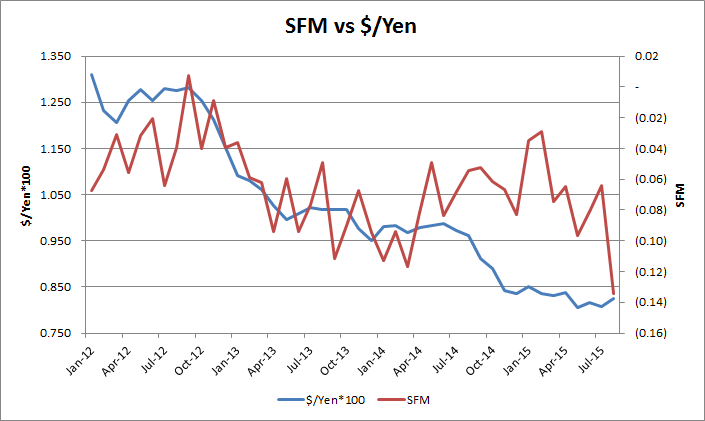

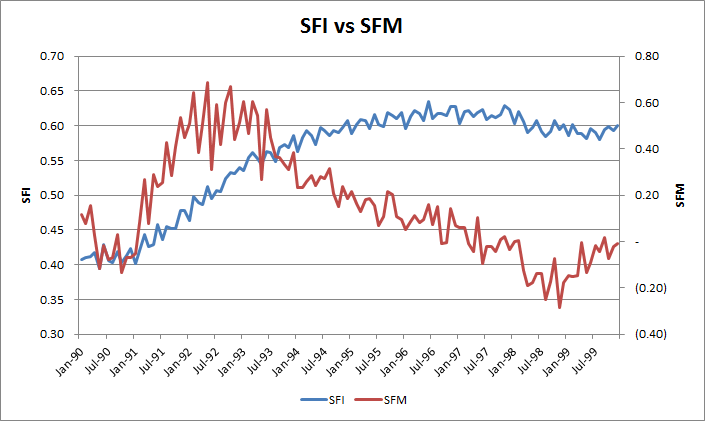

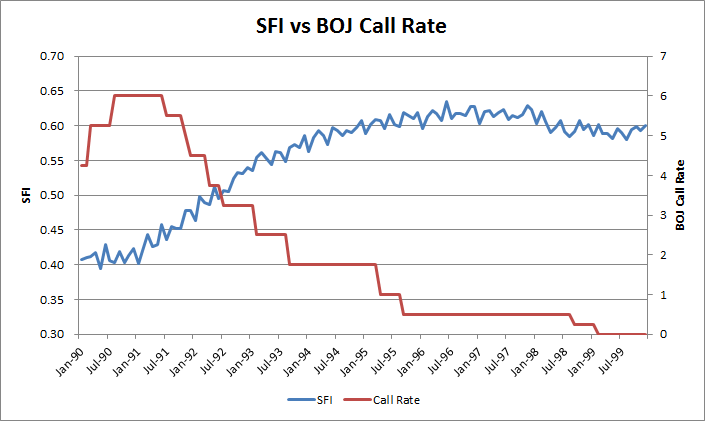

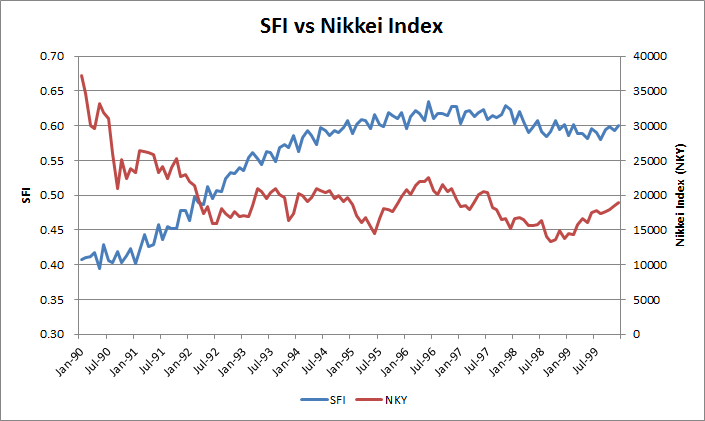

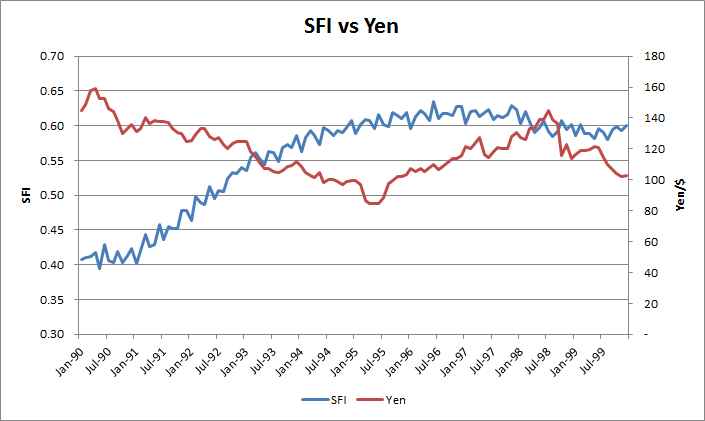

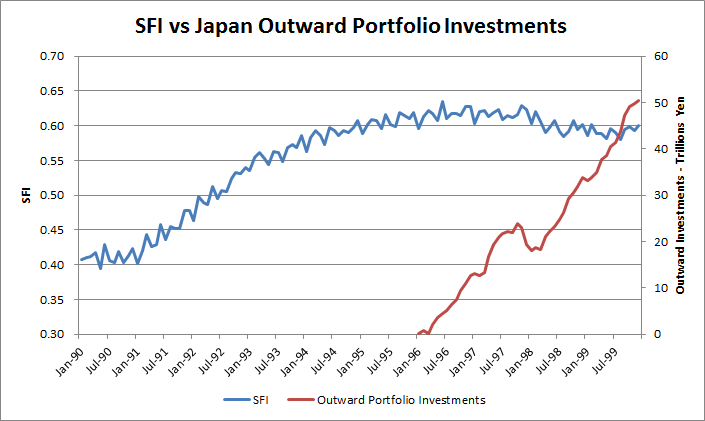

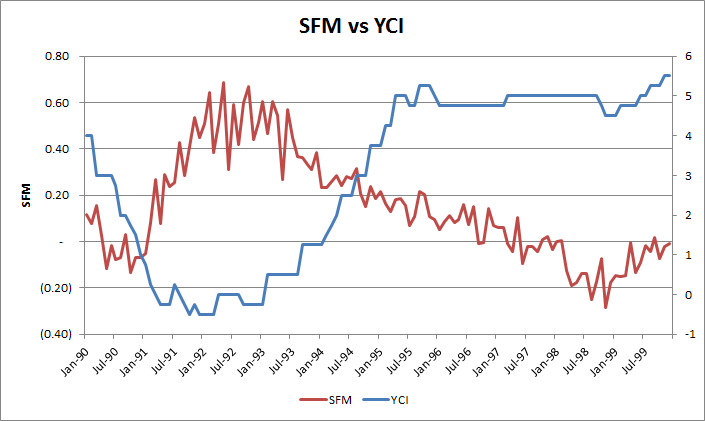

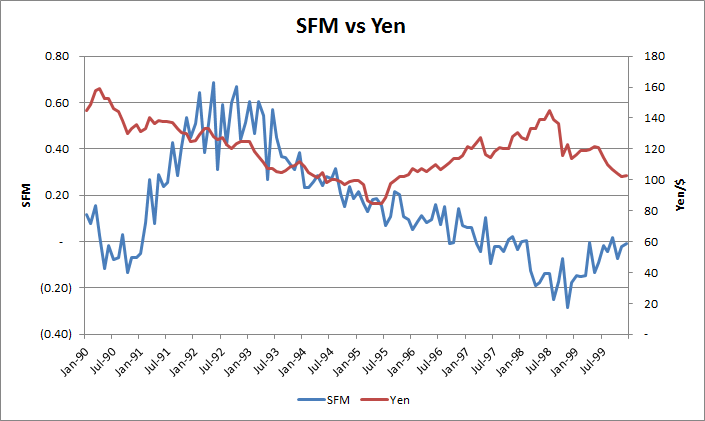

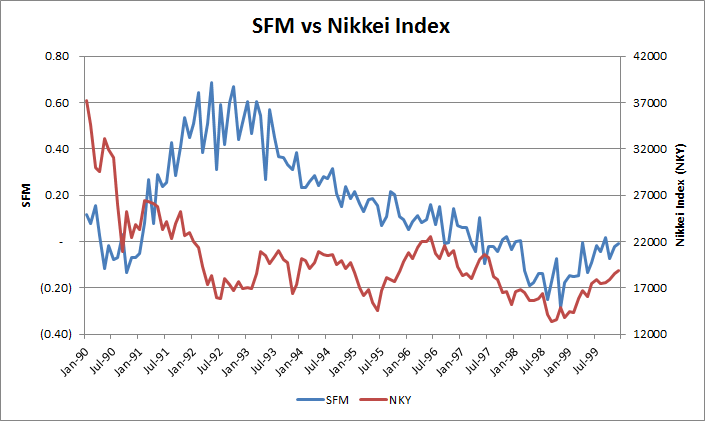

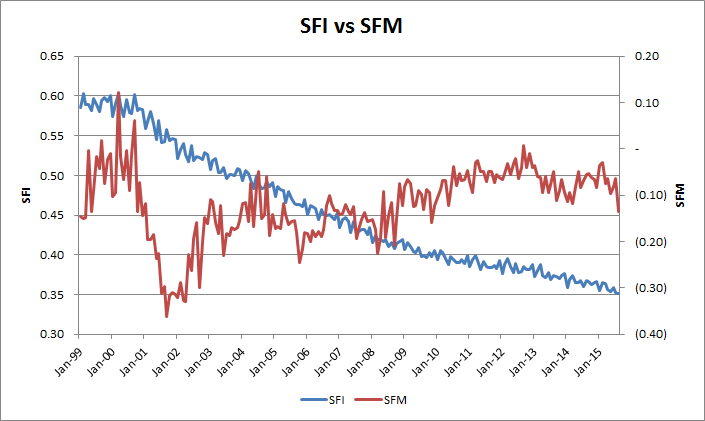

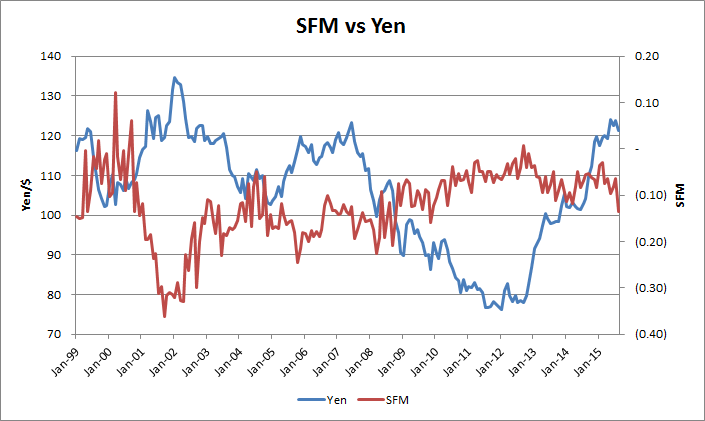

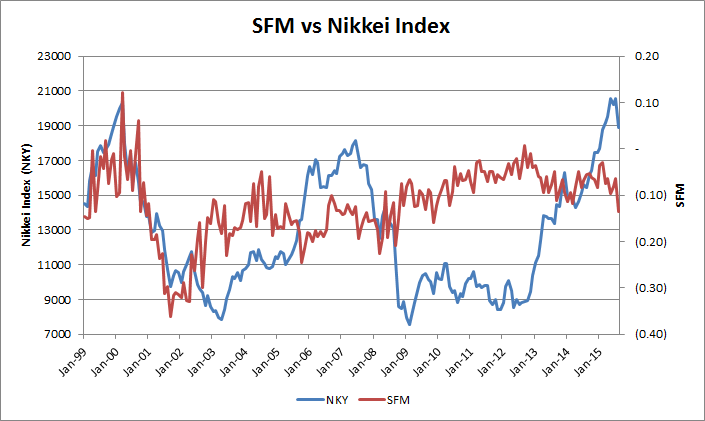

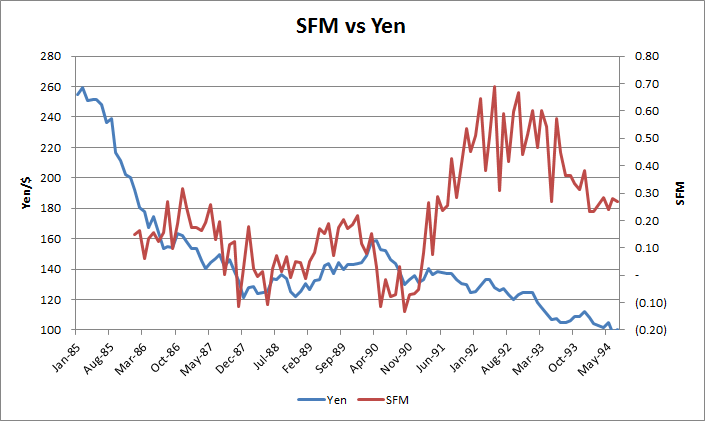

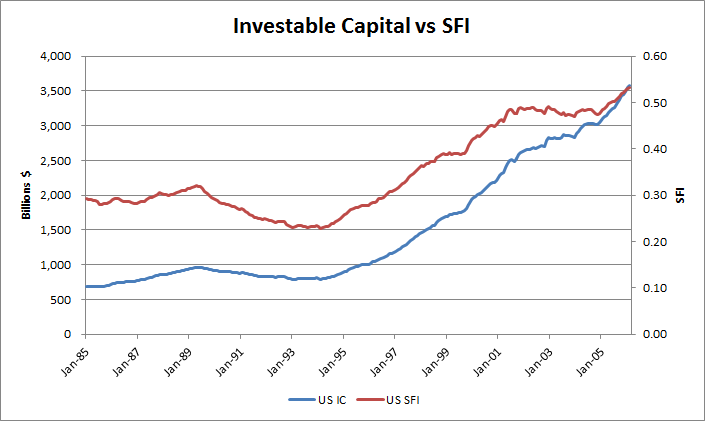

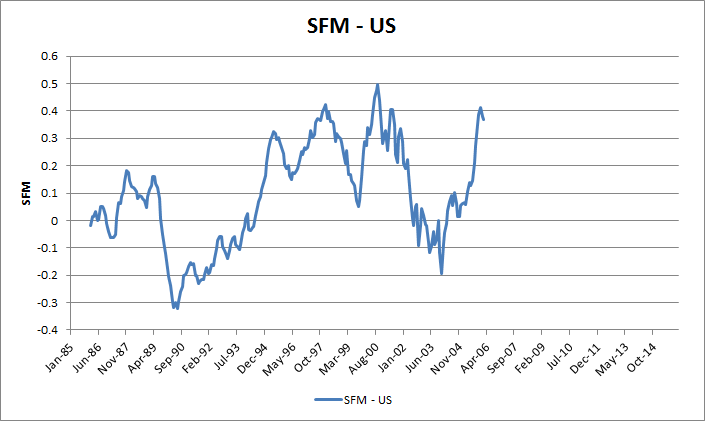

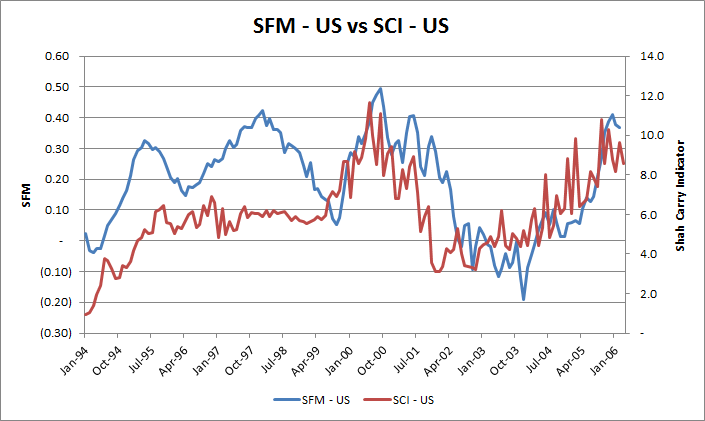

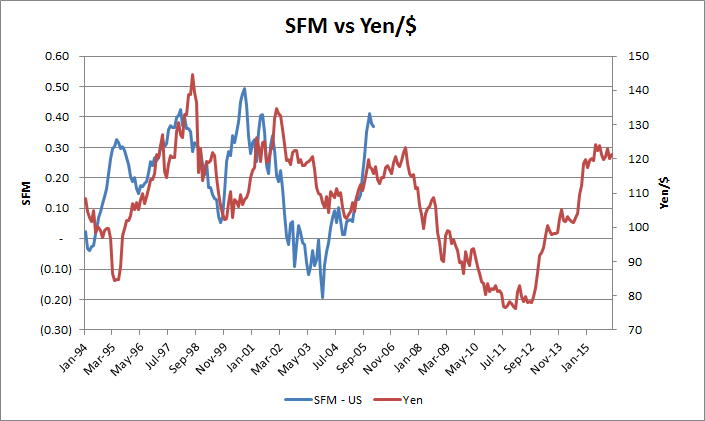

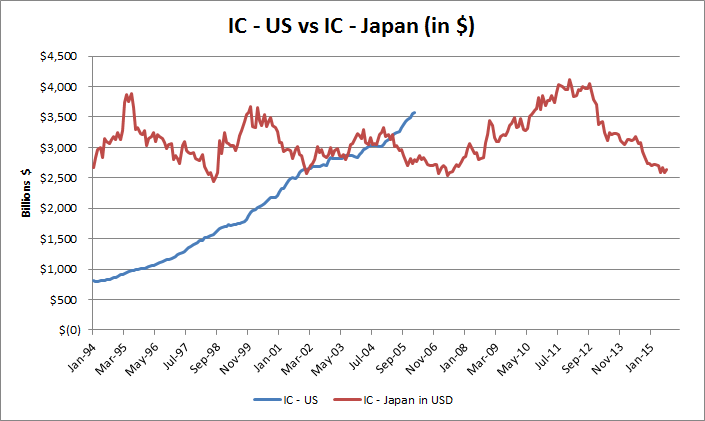

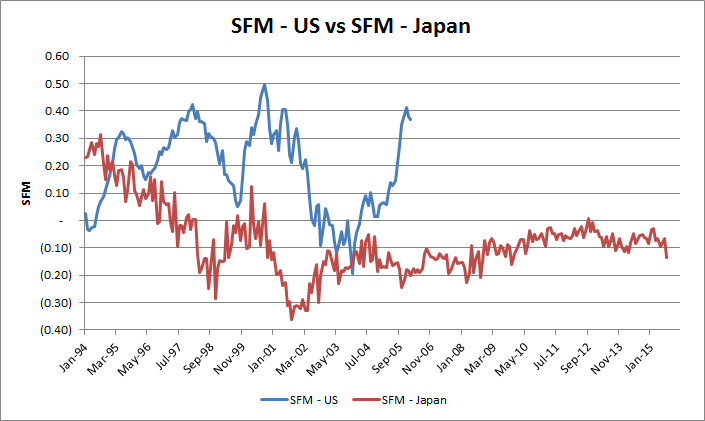

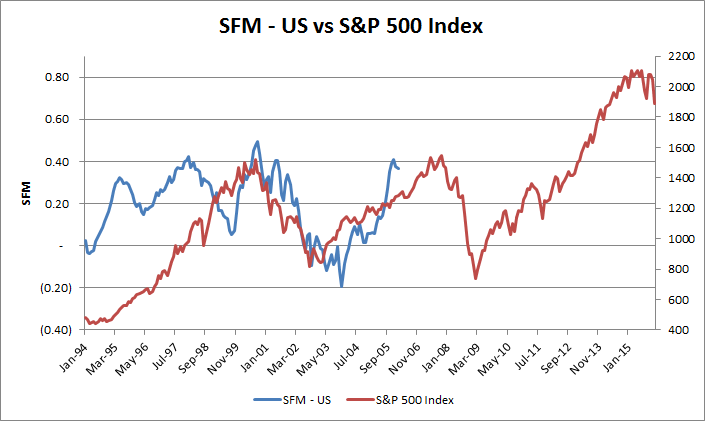

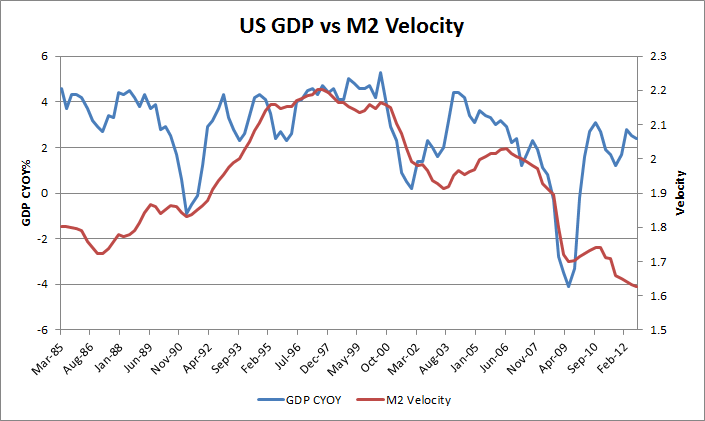

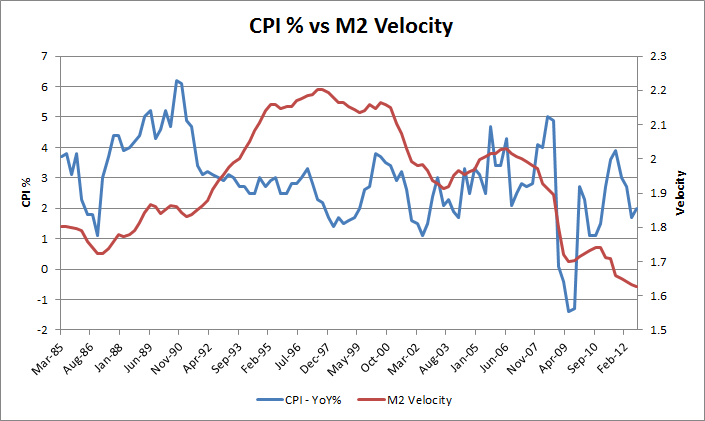

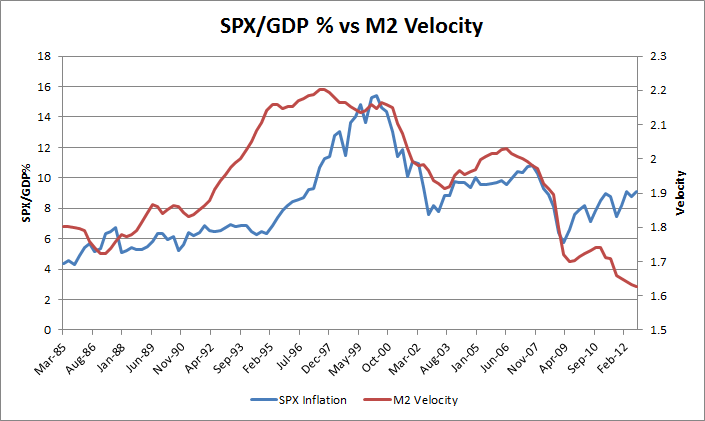

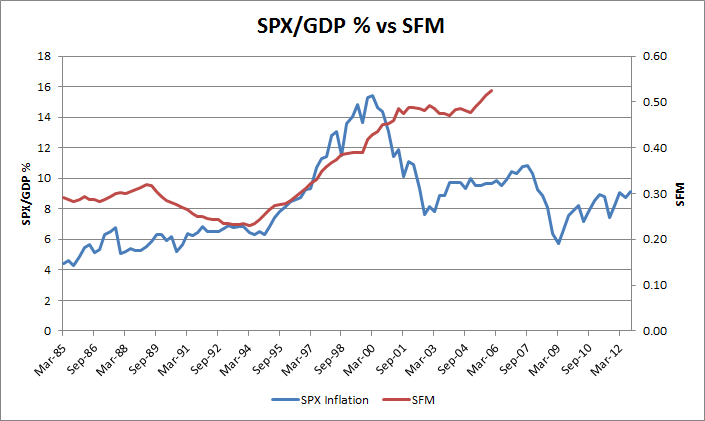

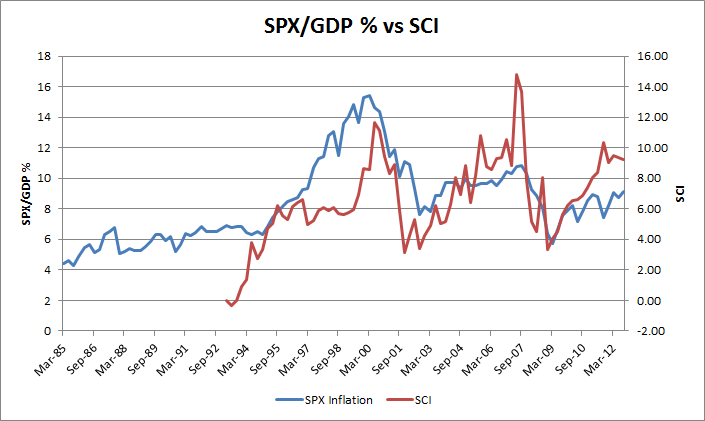

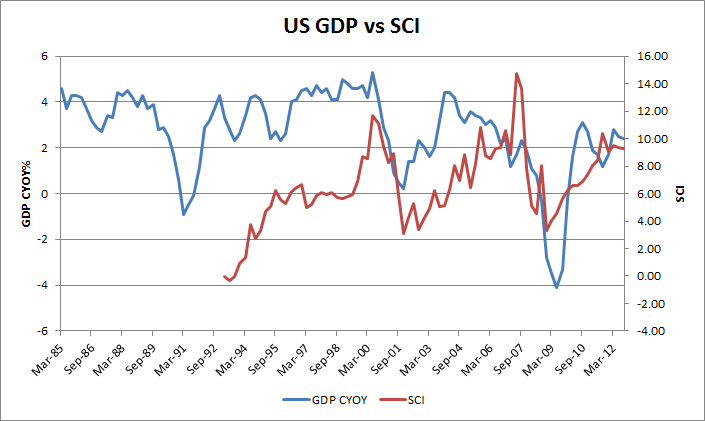

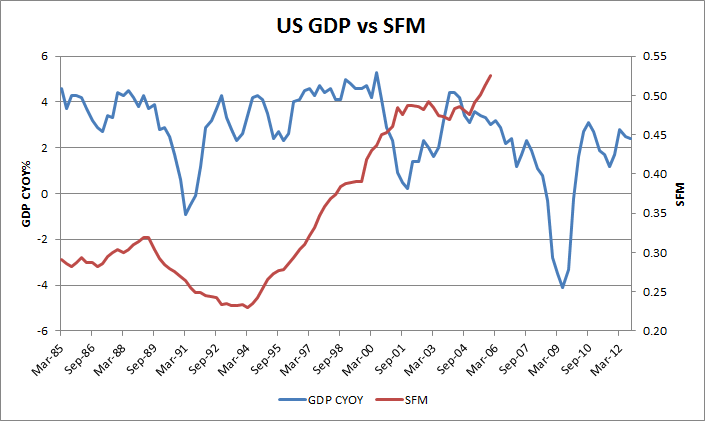

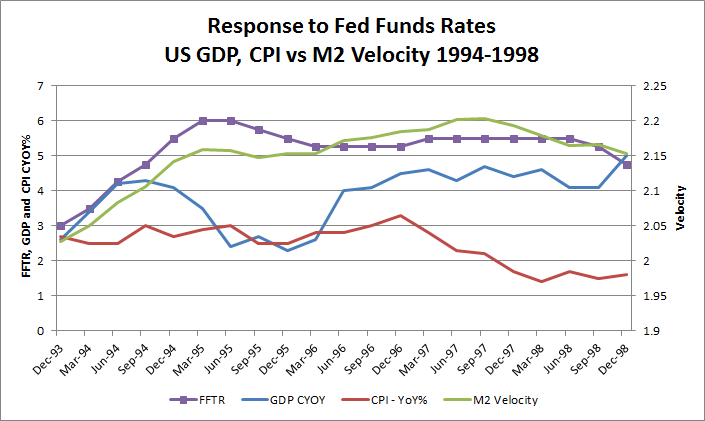

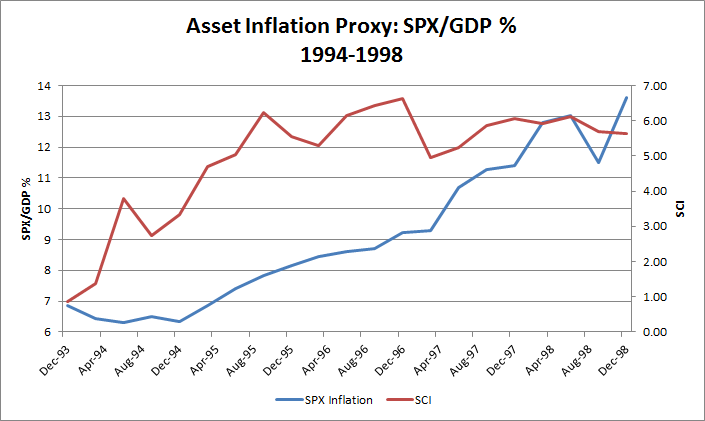

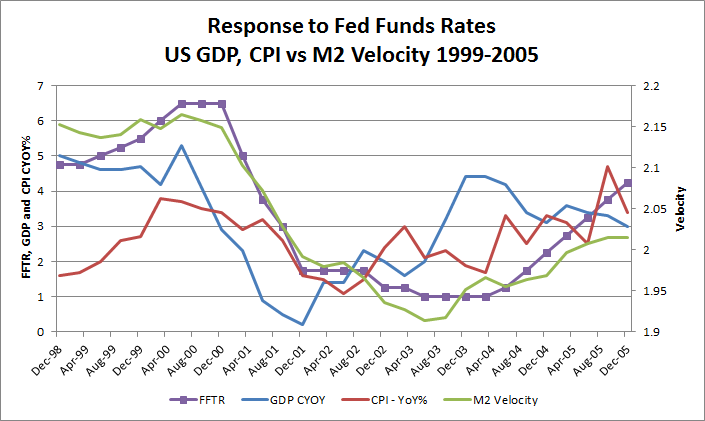

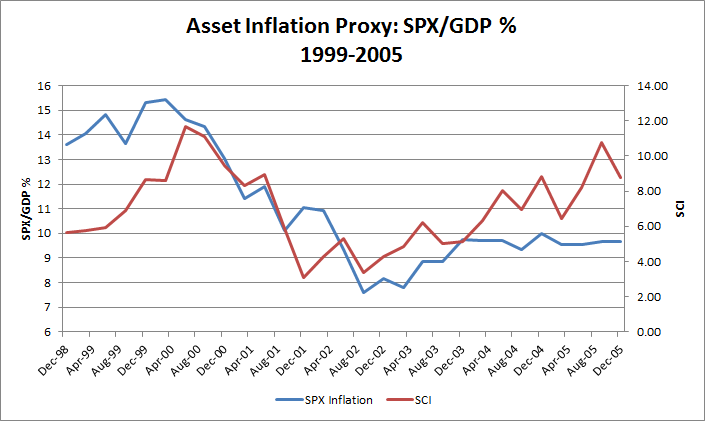

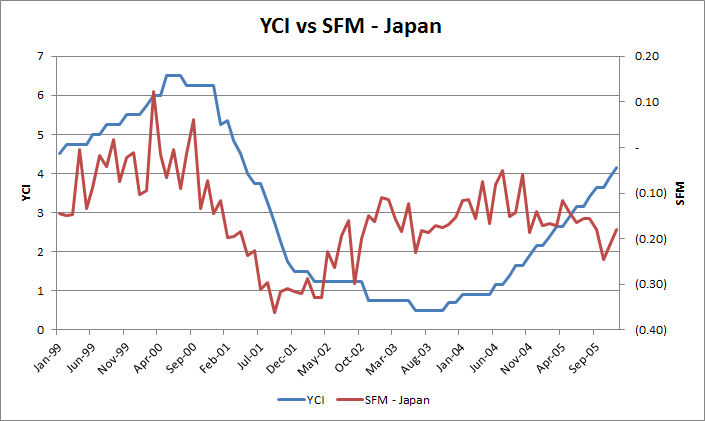

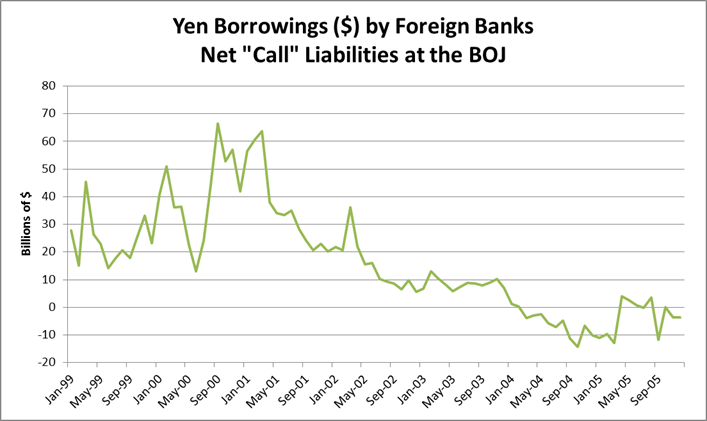

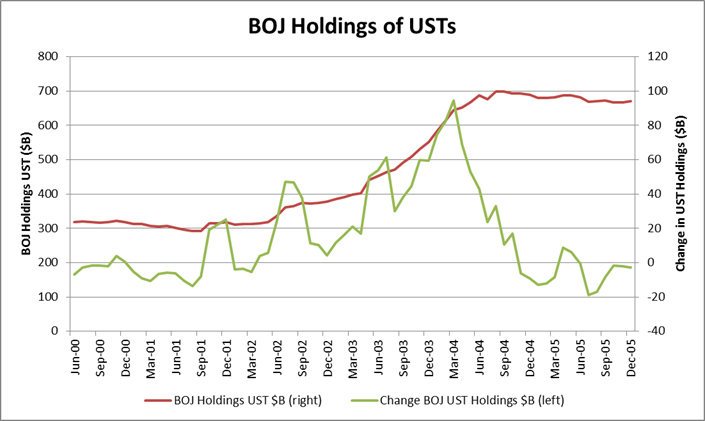

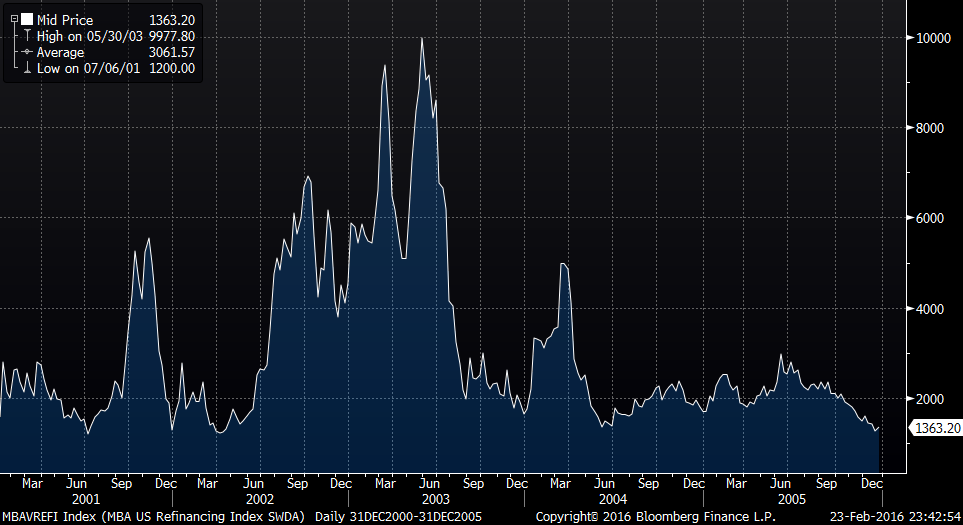

Section 2: The Pricing of AssetsIn this section we will compare the Shah Carry Indicator to a variety of Assets and economic indicators.

While it is widely accepted that asset prices are influenced by money supply, what has changed since 1994 is that the local central bank is no longer the monopoly supplier of money and money supply, and that it is money supply from global sources that determines asset prices, not just local money supply.

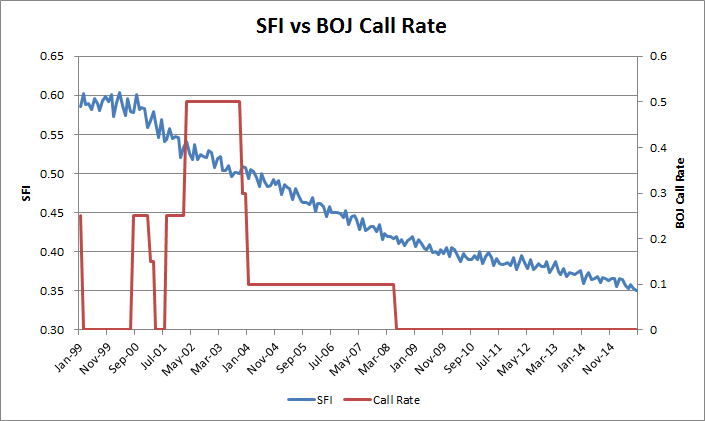

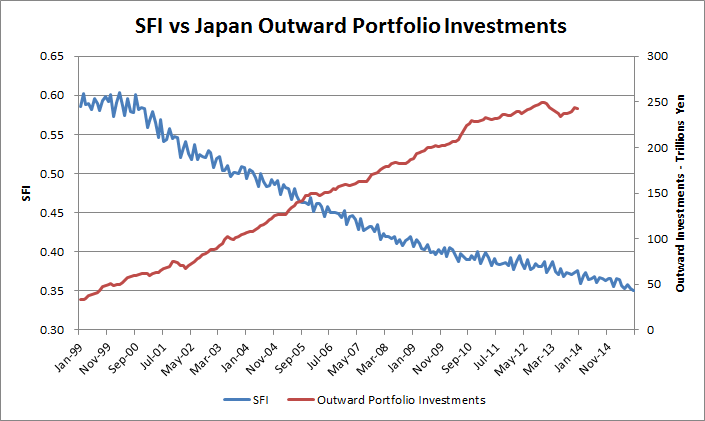

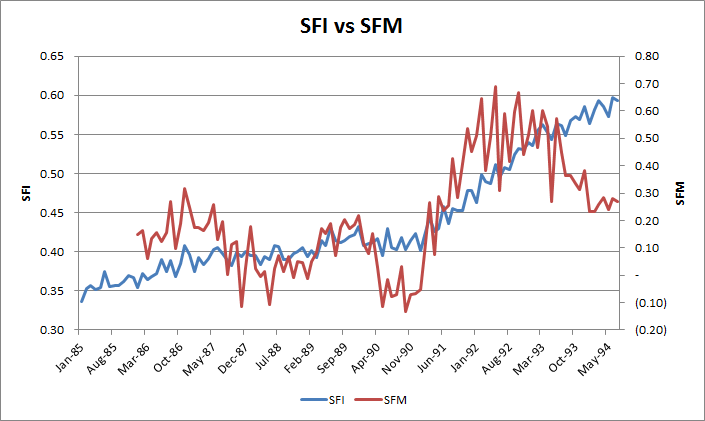

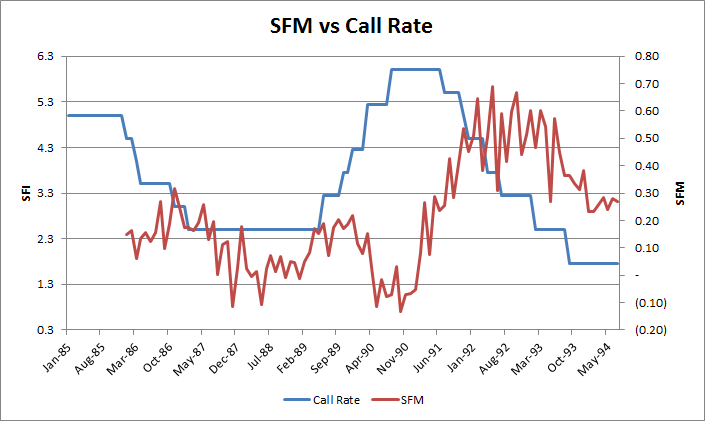

Please don't expect perfect correlations to all assets - there are other factors at work, such as hedge/leverage ratios that move with volatility.

Many of these graphs show that different betas, or sensitivities, apply to different assets. The SCI has some explantory power for the prices of most assets, with greater linkages for financial assets.

{kind=link}

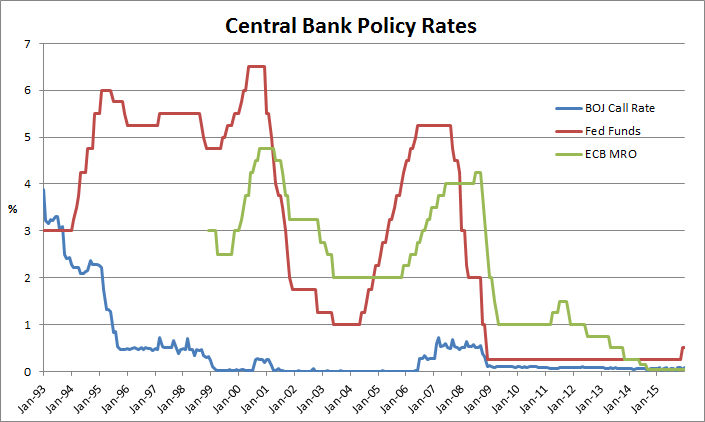

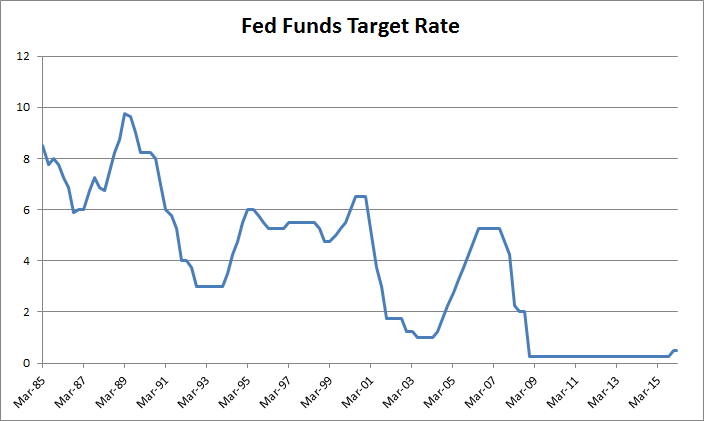

Section 3: The Failure of Macro EconomicsIn this section, I will explain what Central Bankers are attempting to accomplish with Monetary Policy, look at it's effectiveness in today's economic world structure, and look at what they actually do manage to accomplish. I use the examples of the Japanese and US economies, and the policy decisions of each country, in this analysis.

A Summary of Monetary Policy

Central banks mostly attempt to manage money supply in order to control prices and target inflation. Some central banks have other mandates, such as employment targets and currency management, but the tools used are similar.

The ECB has put up a nice chart describing the Transmission of Monetary Policy. So have other sources.

In a prior Crisis Note, I summarized the Bank of England's white paper titled 'The Transmission of Monetary Policy'. I don't agree with it, but it gives a good picture of what central banks believe and are attempting to achieve. Here it is again:

- - Central banks derive their power from the fact that they are monopoly providers of “high powered” money (base money).

- - Central banks choose the price (rate) at which they lend high powered money to the private sector - the Policy Rate eg. Fed Funds Rate or Uncollateralized Overnight Call Rate.

- - This official rate is transmitted to other market rates via the banking system to varying degrees, and impacts assets prices and expectations, as well as the exchange rate.

- - These changes in turn effect spending, savings, and investment behavior, which impacts the demand for goods and services.

- - Monetary policy works via its influence on aggregate demand in the economy. Monetary policy thus determines the general price level, and the value of money i.e. the purchasing power of money. (Inflation is thus a monetary phenomenon. )

- - Changes in the policy rate lead to changes in behavior of both individuals and firms, which when added up over the whole economy generate changes in aggregate spending.

- - Total domestic expenditure in the economy is equal to the sum of private consumption expenditure, government consumption expenditure and investment spending. This, plus the balance of trade (net exports) is equal to GDP.

- - Monetary policy changes affect output and inflation, as well as inflation expectations. - Inflation expectations influence the level of real interest rates and so determine the impact of any specific nominal interest rate. They also influence price and money wage setting, and so feed into actual inflation in subsequent periods.

- - Money supply plays a role in the transmission mechanism of policy, but is not a policy instrument nor a target, as the central bank has an inflation target, and uses monetary aggregates as indicators only.

- - There is a positive relationship between monetary aggregates and the general level of prices. - “Monetary growth persistently in excess of that warranted by growth in the real economy will inevitably be the reflection of an interest rate policy that is inconsistent with stable inflation. So control of inflation always ultimately implies control of the monetary growth rate. However, the relationship between the monetary aggregates and nominal GDP ..appears to be insufficiently stable (partly owing to financial innovation) for the monetary aggregates to provide a robust indicator of likely future inflation developments in the near term.”

- - Shocks to spending can have their origin in the banking system, that are not directly caused by changes in interest rates

- – Examples include declines in bank lending caused by losses of capital on bad loans: a credit crunch.

The tools of Monetary Policy are the Policy Rate, Reserve Requirements, Margin Requirements, and more unconventionally, Quantitative Easing and penalty (negative) policy rates.

Money Supply

There are a number of measures of Money Supply, depending on the country, from 'narrow' to 'broad'. Typically they are defined as follow:

- - M1 is usually a narrow definition - coins and notes in circulation

- - M2 is typically M1 plus short term bank deposits, savings and checking accounts, money market funds, etc.

- - MZM - Money Zero Maturity - A measure of the liquid money within an economy. MZM represents all money in M2 less the time deposits, plus all money market funds

- - M3 is M2 plus longer term deposits

- - Some countries have even broader definitions.

Since Money Stock is relatively constant, each of these measures also has a 'Velocity' associated with it, which needs to be targeted to target inflation - "control of inflation always ultimately implies control of the monetary growth rate" - i.e. Velocity.

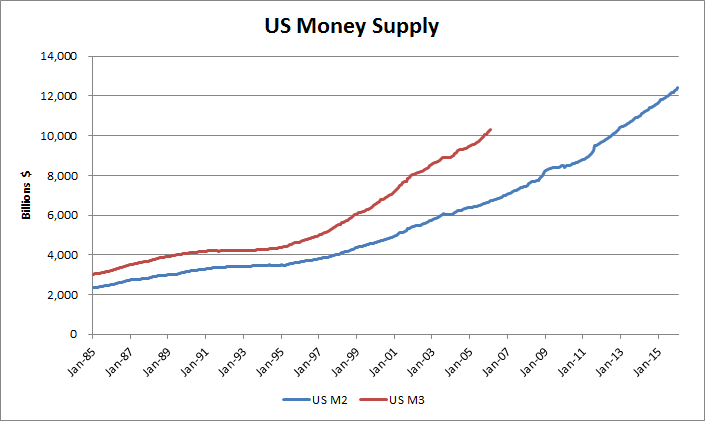

What is especially annoying is that the US Fed, in 2006, stopped measuring and publishing M3. I find this very suspicious, as I believe that the DIFFERENCE between M3 and M2 is critical for understanding the monetary forces at play in the economy. The public reason for not measuring M3 anymore was to save money, since the Fed claims that M2 explained everything they needed, and M3 did not add any more explanatory power. To which I answer: "Rubbish", along with some more colorful words.

As you will see later, M3-M2 was on a rocket-like vertical trajectory in 2005-2006. My speculation is that the Fed could not or did not want to explain this, resulting in the cancellation of M3. Had they looked at it more closely, they would have spotted the Financial Crisis brewing. I need to see if they published the minutes of the meeting leading to the cancellation of M3, or whether it was done more surreptitiously.

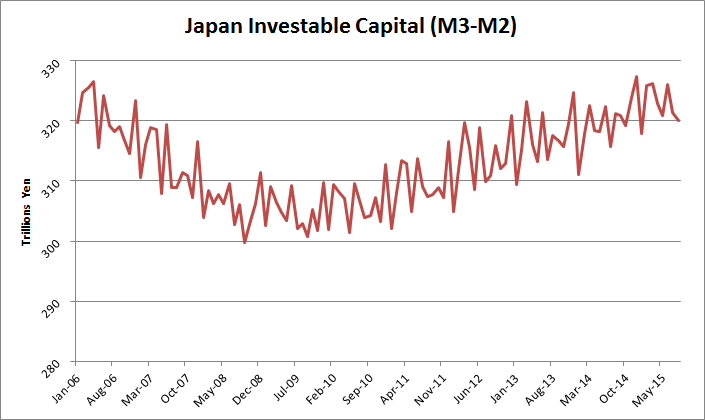

Japan, on the other hand, also has problems with it's M2 and M3 data. The current official measurements were changed in 2003. The prior M3+CD series ended in 2008, and the prior data I have found from other sources is not 'good' - the OECD Japan M3 specifically looks doctored. The data makes it hard to get a good long term view of the issues.

Quantity Theory of Money

Simplistic, but good enough to understand central bank thinking.

MV = PQ

M = quantity of money

V = Velocity

P = Price Level

Q = Real GDP - quantity of real goods sold

Since M is usually stable, increasing Velocity will lead to inflation in P, and often, more resources allocated to increasing the quantity of real goods produced. Alternatively, you can increase M by printing money or increasing the Money Supply (QE is one way).

To generate Velocity of Money, the banking system is necessary and critical, as velocity is generated through the Fractional Reserve banking system, through Loans for Productive uses that then recycle back through the economy.

So, to generate Velocity, Lending is important, as is Productive goods production.

A criticism of the Quantity Theory of Money comes from Paul Samuelson (in reference to assumptions about velocity).

In terms of the quantity theory of money, we may say that the velocity of circulation of money does not remain constant. “You can lead a horse to water, but you can’t make him drink.” You can force money on the system in exchange for government bonds, its close money substitute; but you can’t make the money circulate against new goods and new jobs.

As an alternative, I describe the IS-LM model in this Crisis Note, but you can refer to any Macro Economics textbook. The objectives are similar - Policy Interest Rate management is used to increase money supply through velocity of money.

Targets of Monetary Policy

- * Inflation Target

- There are 3 types of inflation that matter

- - Goods Price Inflation

- - Wage Inflation

- - Asset Inflation

- * Full Employment

- - measuring employment and unemployment is a favorite sport of economists

- - the headline unemployment number does not represent reality

- * GDP growth

- - we need to look into the components of GDP growth.

- - it is relatively easy for an administration to increase the size of government, but if it is not productive, it will not lead to Velocity of money.

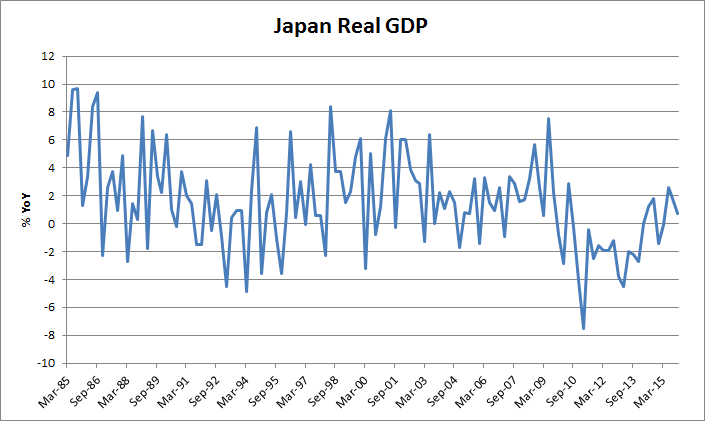

Part 3A: Japan

Japan's Failure to Achieve Desired Results from Keynesian Macro Economic Policies

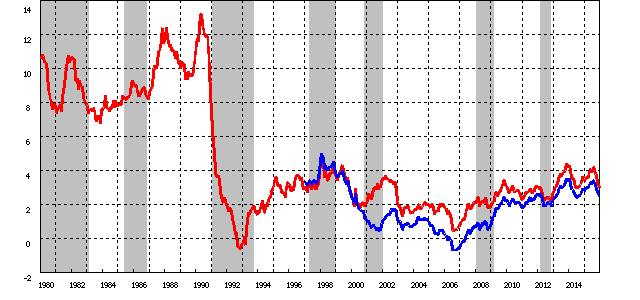

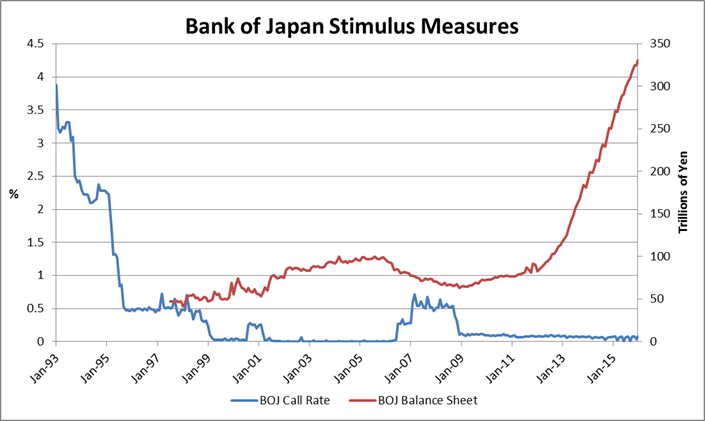

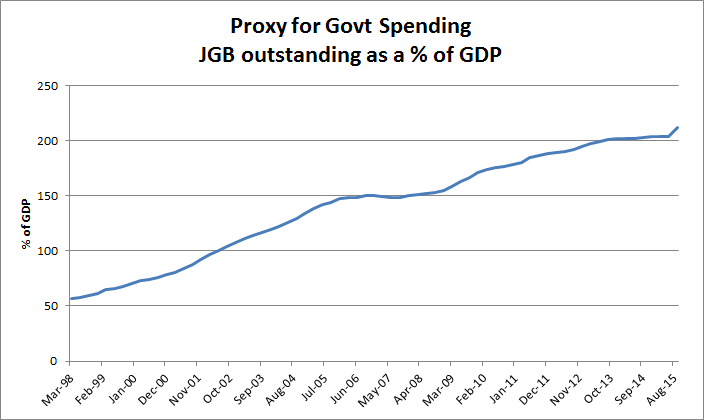

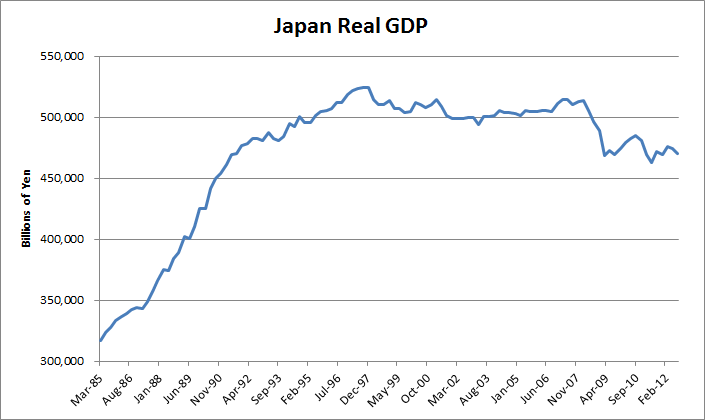

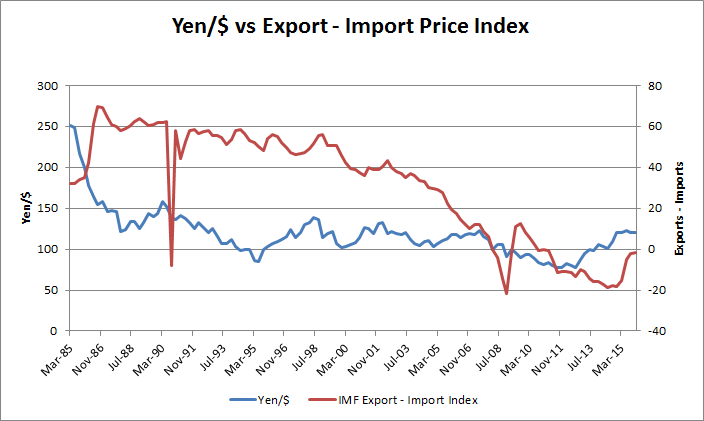

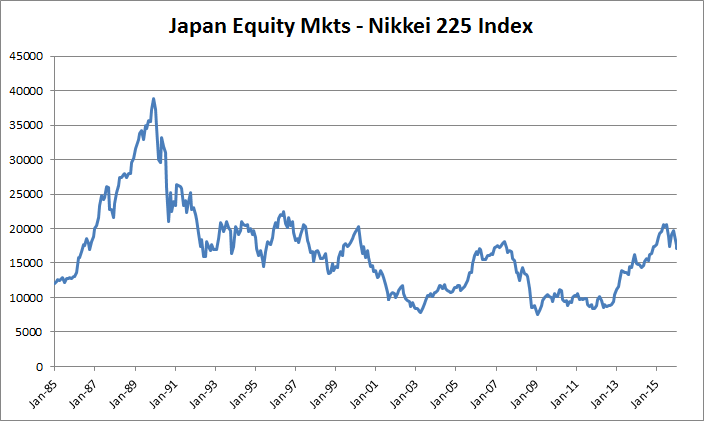

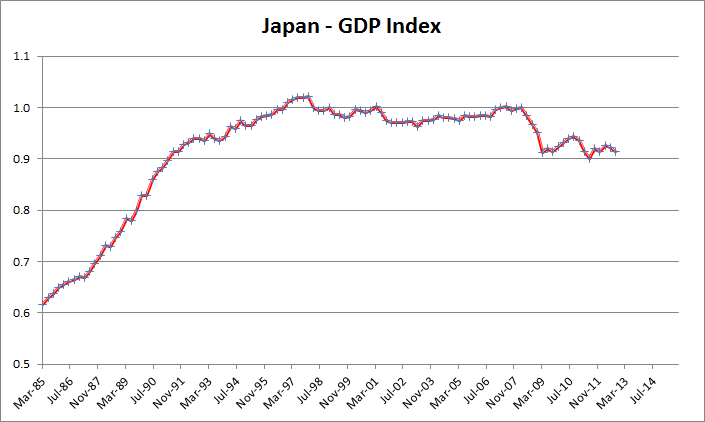

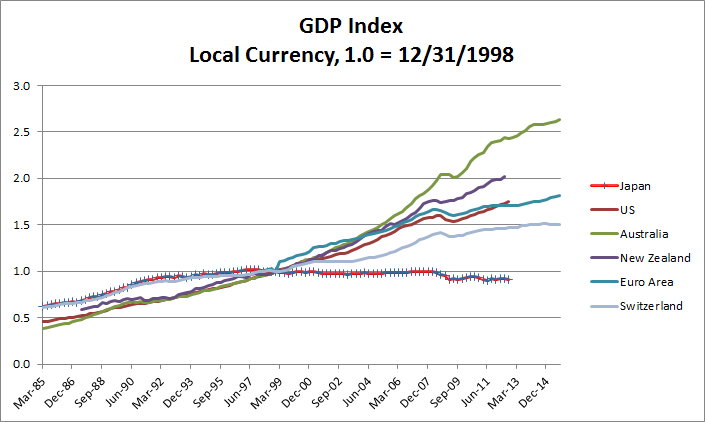

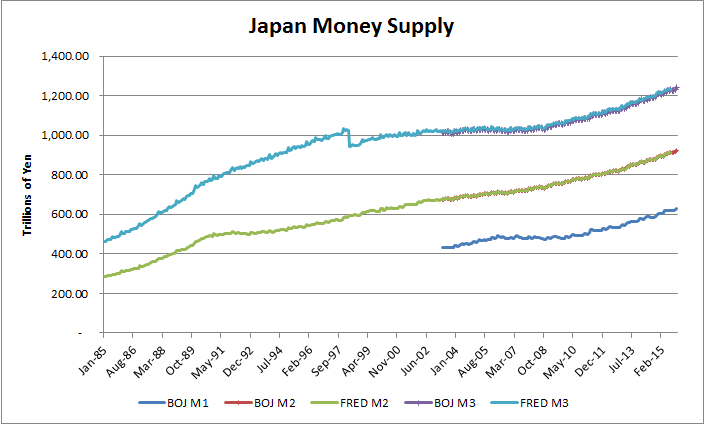

As desribed above, Japan entered a recession in 1984-1985, and has been struggling to get out of it every since. While official statistics show 6 different recessionary periods since then, in my opinion the entire period from 1989 to the present has been defined by the collapse in the measures of money - M2 and M3 - in 1989. Since then, the BOJ, and the government, have tried every play and trick in the economist's handbook, with limited to negative success.

Here is the official BOJ Japan Money Supply chart with Recession Periods marked.

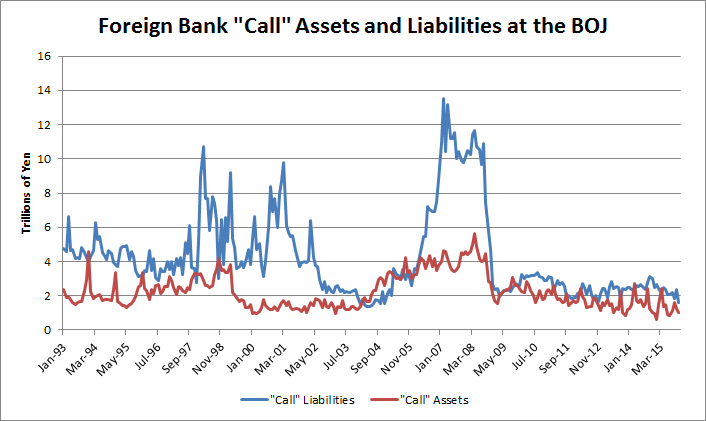

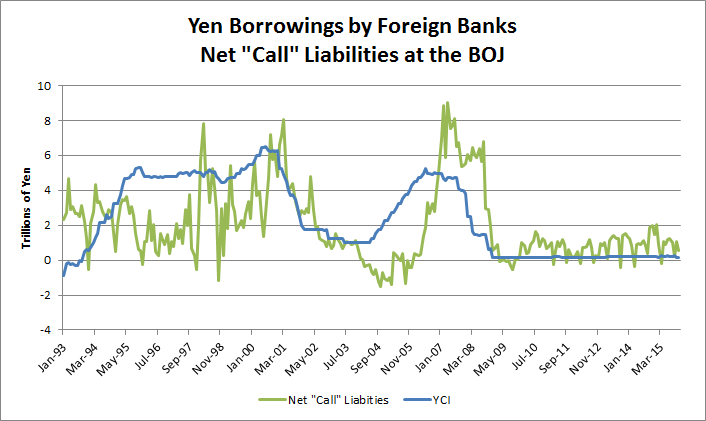

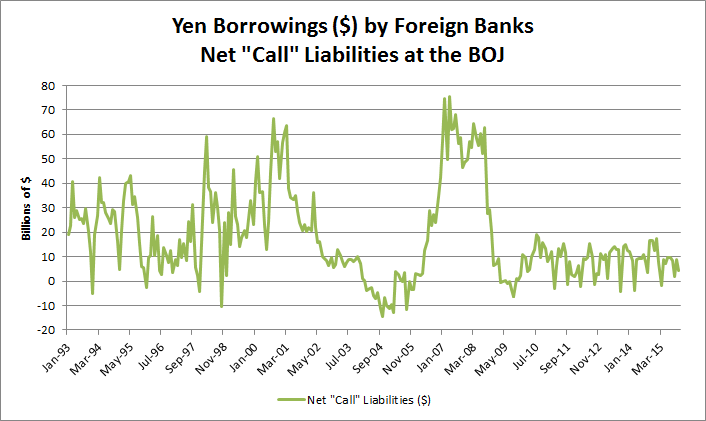

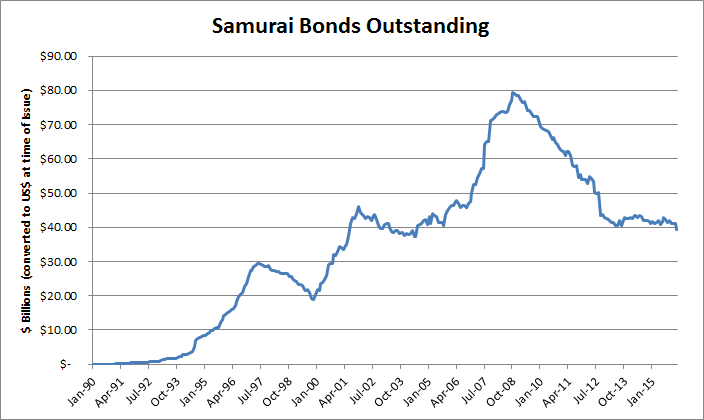

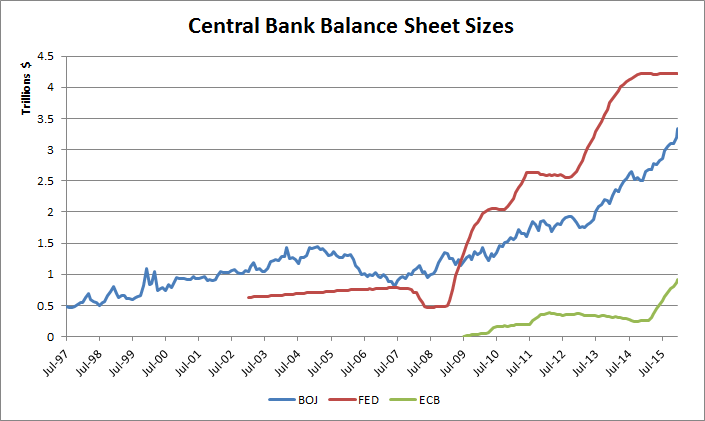

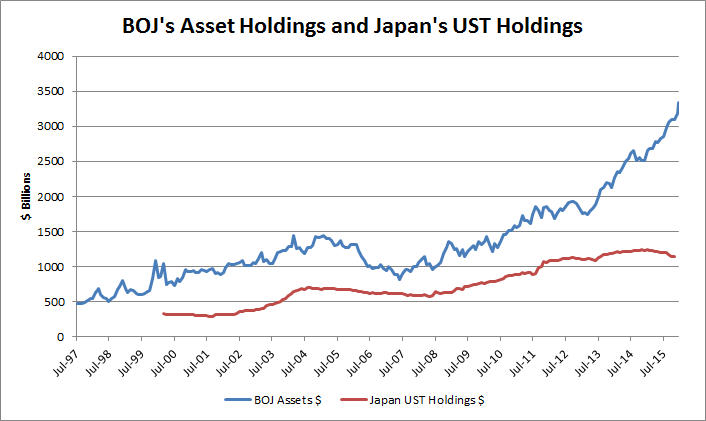

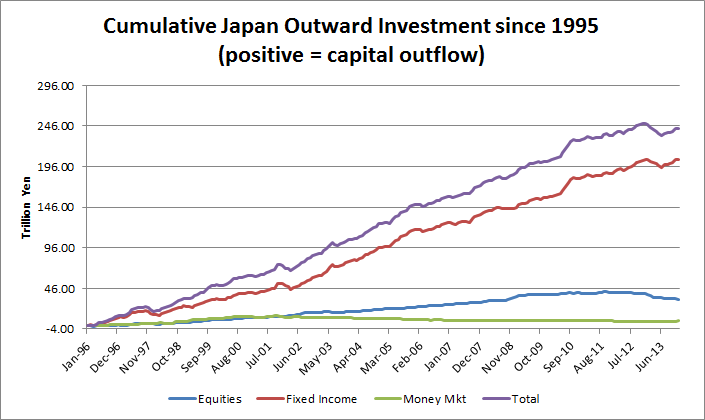

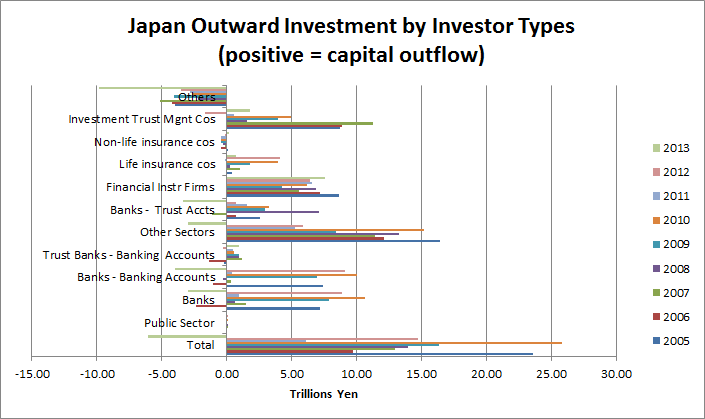

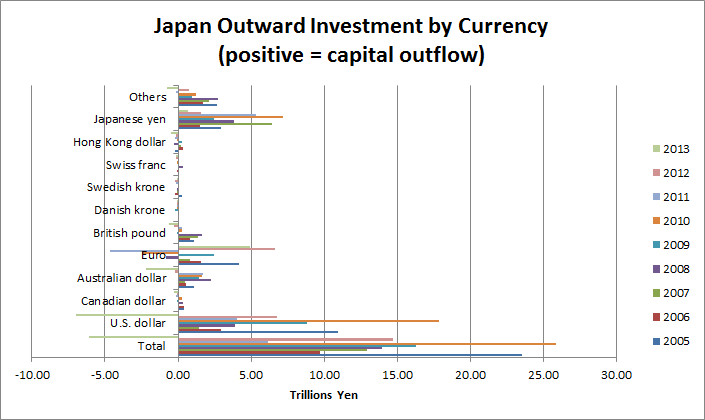

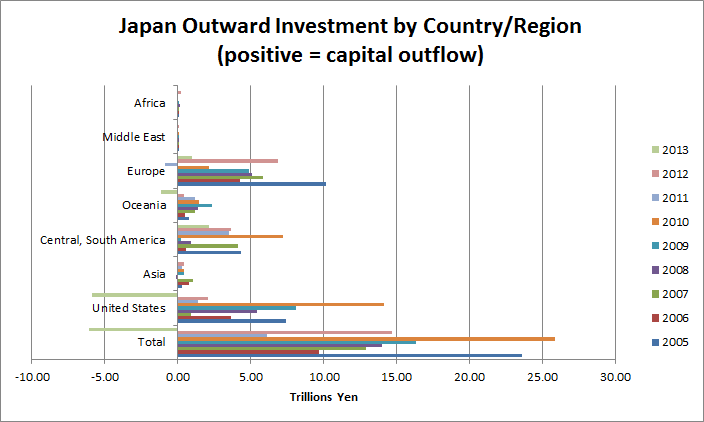

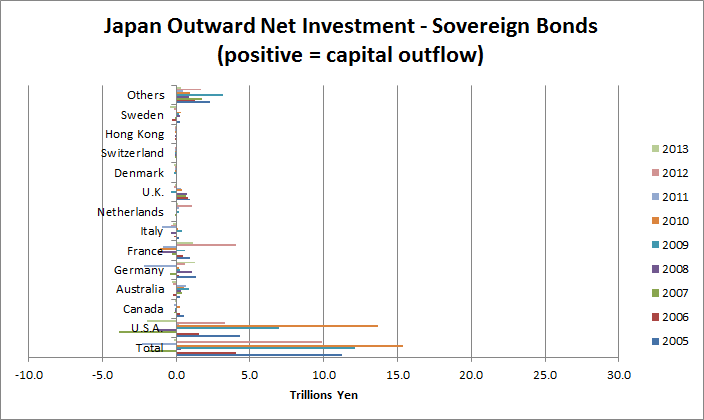

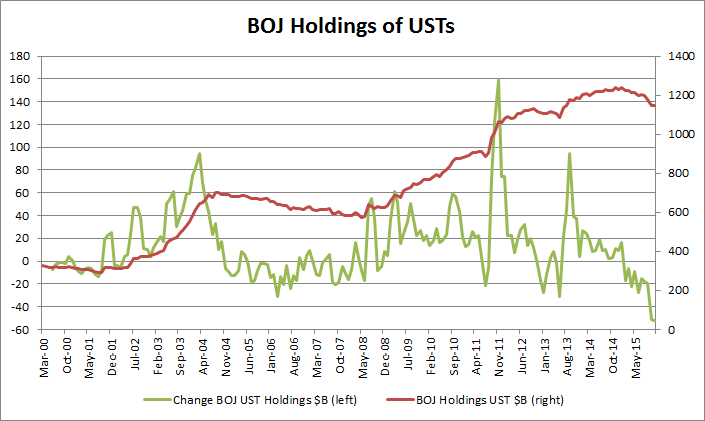

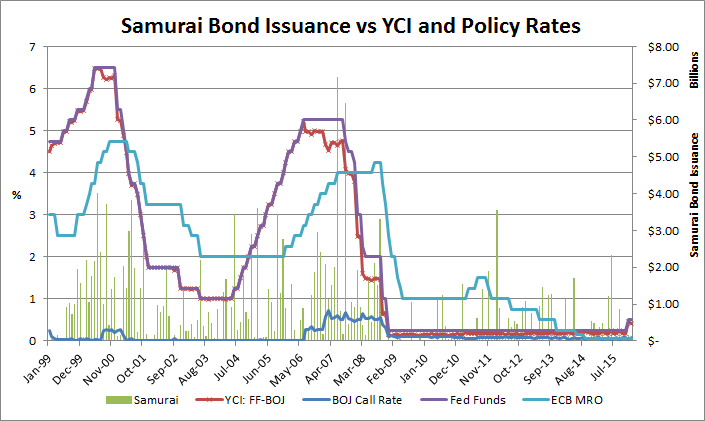

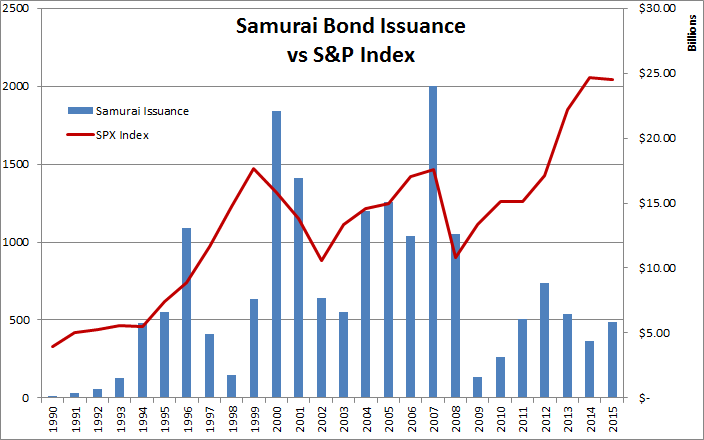

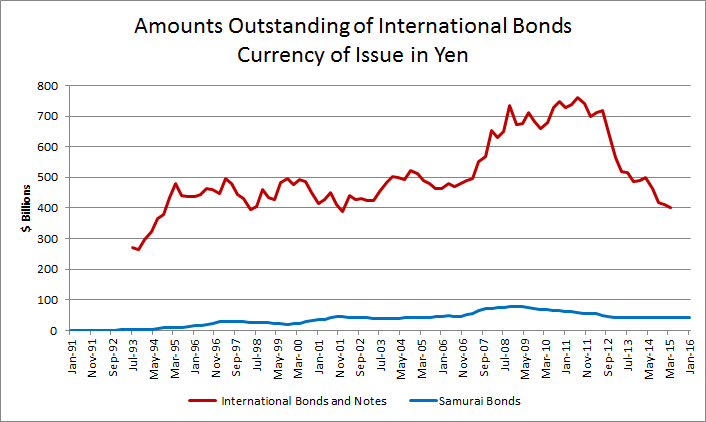

I have figured out how to estimate the total amount of Japanese capital and money supply exported to the US. I estimate this at at least $1.5T in 2007, and it is the withdrawal of this money supply and leverage from the US was primarily responsible for converting a US mortgage crisis into a Global Financial Crisis. More on this later.

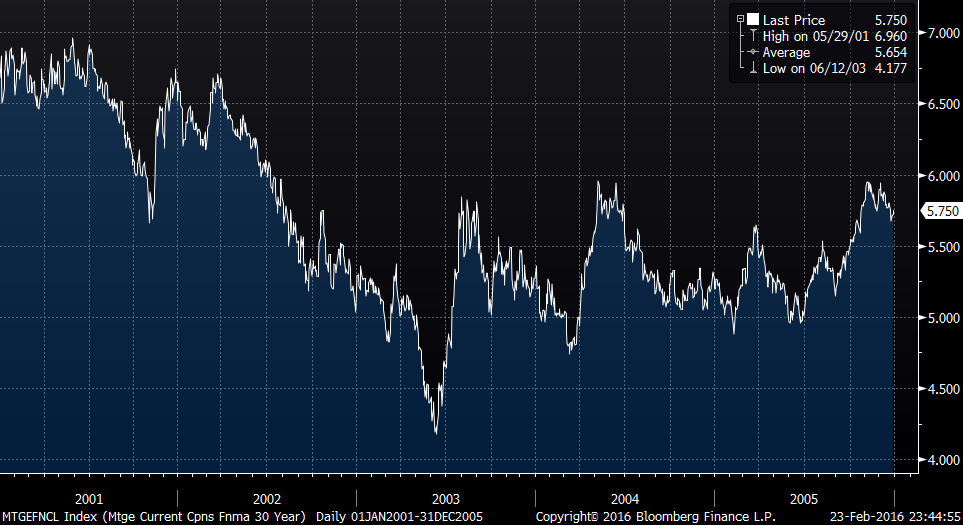

Daily 12-26-00 to 12-31-01.png)

Daily 12-26-00 to 12-31-05.png)

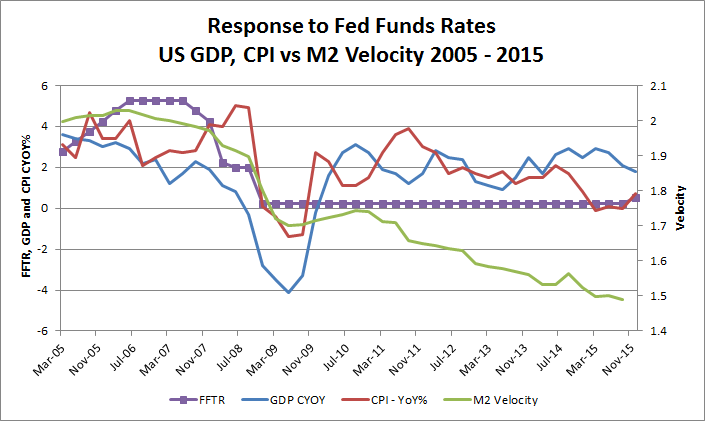

Dai 2016-02-23 23-40-57.png)

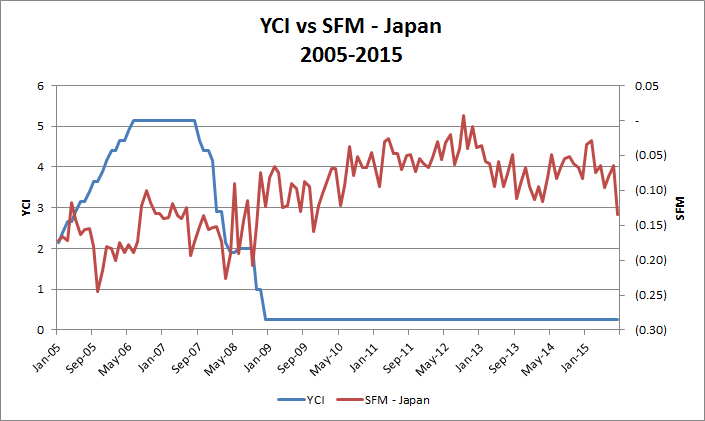

2016-02-24 10-19-48.png)

2016-02-24 10-41-39.png)

Daily 2016-02-24 11-16-37.png)

Daily 2016-02-24 11-26-43.png)